The Dollar Just Learned How to Obey Orders

A quiet morning. Someone orders a coffee—medium roast, oat milk, no sugar. The payment goes through instantly. A tap of the phone, a gentle beep, transaction complete. Smooth. Invisible. Frictionless.

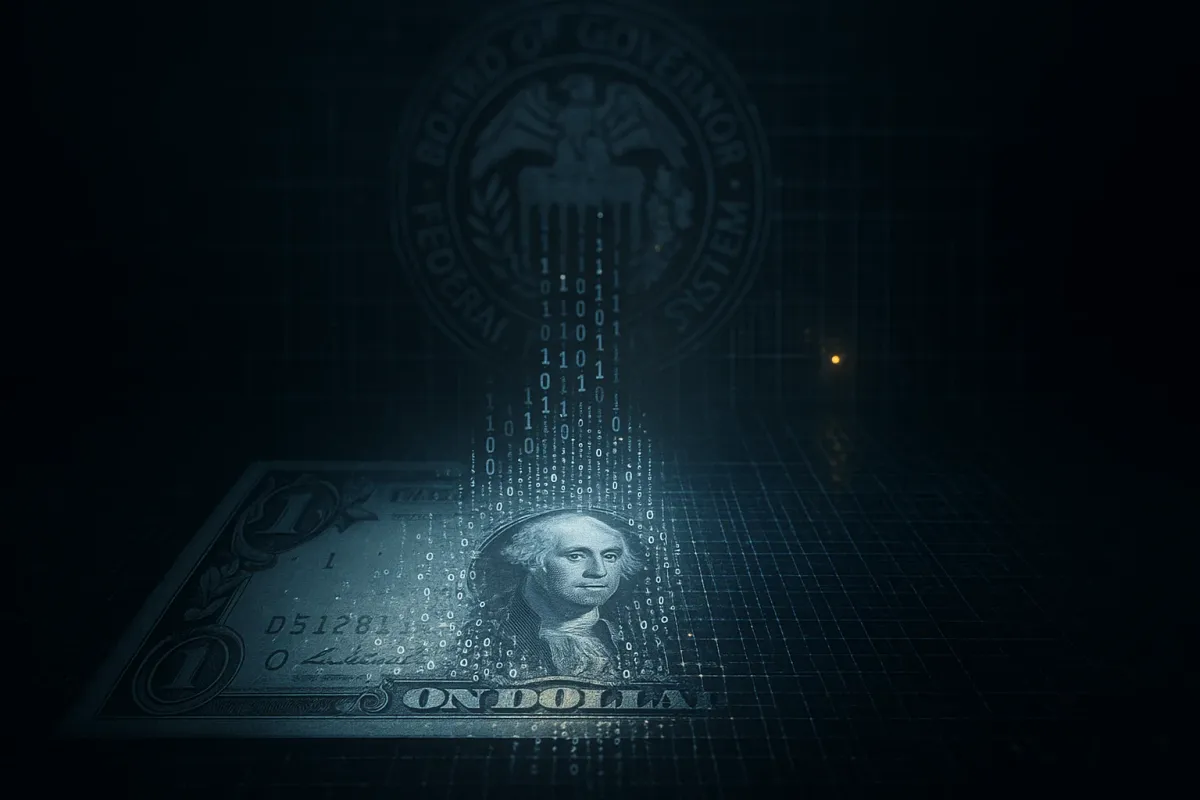

But somewhere in a server farm outside Washington D.C., that purchase is logged, timestamped, categorized. The algorithm notes the location, cross-references spending patterns, and files the data alongside thousands of other transactions from the same user. It doesn't judge. It just records.

This is the new economy—one that doesn't forget, doesn't lose receipts, and never stops watching.

And most people don't realize the infrastructure is already built.

The Hidden Shift in Plain Sight

While Americans spent 2023 and 2024 arguing about inflation rates, interest hikes, and whether we'd hit recession, Washington was building something far more consequential: the digital rails for programmable money.

It didn't come with a press conference. There was no primetime address explaining that the government was preparing to replace physical currency with a traceable, controllable digital alternative. Instead, it arrived piecemeal—buried in regulatory updates, pilot programs, and infrastructure upgrades that sounded technical and boring.

FedNow, launched in July 2023, was sold as a faster payment system—real-time transfers, 24/7 availability, instant settlement. Convenient. Modern. Efficient. But beneath the consumer-facing promises, FedNow built the backbone for something larger: a centralized payment infrastructure where every transaction can be monitored, flagged, or blocked in real time.

Then came the CBDC pilot programs—quietly announced, minimally covered, operating in partnership with select banks and fintech companies. The official narrative: "exploring options," "improving financial inclusion," "keeping pace with innovation." The reality: testing the systems required to roll out a Central Bank Digital Currency (CBDC) at scale.

By the time most Americans noticed, the infrastructure was already operational. The shift wasn't coming. It was already here.

Once this digital dollar goes live, the government will have complete control over your money:

- They’ll see every dollar you spend.

- They’ll decide what’s “approved.”

- They can even freeze your account with one click.

That’s not financial freedom. That’s financial surveillance.

But here’s the good news — you still have time to legally opt out before it’s too late.

A new report just dropped that shows how Americans are using a simple, IRS-approved move to shield their savings with real gold and silver. Physical assets that can’t be tracked, deleted, or controlled by policy.

The Mechanics of Control

A CBDC isn't Bitcoin. It's not Ethereum. It's not even close to decentralized cryptocurrency.

Here's the fundamental difference: every transaction in a CBDC system passes through government gateways.

With cash, you hand someone a $20 bill. No record. No intermediary. No trace. The transaction is peer-to-peer, anonymous, final.

With cryptocurrency (if used correctly), transactions occur on decentralized networks. Transparent, yes—but pseudonymous. No central authority controls who can send or receive.

With a CBDC, every payment is centralized, traceable, and programmable. Here's what that means in practice:

- Full traceability: The government knows who you paid, when, how much, and what category the purchase falls under (groceries, fuel, healthcare, entertainment). Aggregated over time, this creates a complete financial profile.

- Programmable restrictions: Money can be coded with rules. Stimulus payments that expire if not spent within 30 days. Fuel allowances that cap how many gallons you can buy per month. "Sin taxes" applied automatically to alcohol or fast food purchases.

- Instant account freezes: No court order required. No due process. If your account is flagged—rightly or wrongly—it can be frozen remotely, instantly, without warning. You can't pay rent, buy food, or access savings until someone decides to reverse it.

The efficiency is real. But so is the control.

| System | Control Level | Privacy | Stability | Government Access |

|---|---|---|---|---|

| Cash | Low | High | Moderate | Minimal |

| CBDC | Total | None | High (Controlled) | Full |

| Gold/Silver | None | High | High | None |

This table isn't speculation. It's structure. Cash offers privacy and independence but is being phased out globally. CBDCs offer stability and efficiency—but at the cost of total surveillance. Tangible assets like gold and silver remain outside the digital grid entirely, which is why they're increasingly attractive to those watching the shift unfold.

The Real-World Parallels: It's Already Happening

This isn't hypothetical. It's operational in multiple countries, and the patterns are unmistakable.

China's Digital Yuan:

Launched in 2020, now used by hundreds of millions. The system tracks every transaction in real time. The government can see what you buy, where you go, and how you spend. Reports from users confirm that certain purchases—politically sensitive books, VPN services, foreign currency—are flagged or blocked. The efficiency is undeniable. So is the control.

The EU's Digital Euro:

In pilot phase, with rollout expected by 2026. Officials emphasize "privacy by design," but regulatory documents reveal that all transactions above a certain threshold will be reportable to tax authorities, and the system architecture allows for programmable spending limits if deemed necessary during economic emergencies.

Canada's Account Freezes (2022):

During the trucker protests, the Canadian government invoked emergency powers to freeze bank accounts of protesters and donors—without court orders, without trials. The mechanism already existed in the banking system. A CBDC would make it instantaneous, requiring no cooperation from banks. Just a keystroke.

The pattern is global. The infrastructure is being normalized. And the argument is always the same: "It's for security. It's for efficiency. It's for your protection."

The American Response: Opting Out While You Still Can

Americans are starting to notice. Not all of them. Not even most. But a growing cohort—libertarians, financial privacy advocates, ordinary savers who've watched the patterns—are quietly repositioning.

The strategy isn't protest. It's exit—moving wealth into assets that exist outside the digital grid.

- Physical gold and silver: Tangible, portable, universally recognized stores of value that no algorithm can freeze or devalue by decree.

- Self-directed IRAs holding precious metals: Legal structures (like IRS Section 408(m)) that allow retirement funds to be held in physical assets, outside traditional brokerage control.

- Non-custodial cryptocurrency: For those who understand the tech, holding crypto in private wallets (not on exchanges) offers a parallel financial system the government can't easily access.

- Cash reserves: Keeping physical currency on hand while it's still legal and functional—because once the CBDC becomes mandatory, cash may be phased out entirely.

This isn't paranoia. It's diversification—the recognition that systems evolve, and those who understand the direction early retain autonomy longer.

The Moral Pivot: Efficiency vs. Permission

There's a moral dimension to this shift that gets lost in technical discussions.

A digital dollar promises efficiency. Instant payments. Lower costs. Reduced fraud. Financial inclusion for the unbanked. These aren't lies. They're real benefits.

But what it really buys is permission.

Permission for the government to see everything you buy.

Permission to restrict what you can purchase.

Permission to freeze your savings if you're flagged—correctly or not.

Permission to program money so it expires, limits your choices, or punishes behaviors deemed undesirable.

Efficiency without privacy isn't progress. It's surveillance disguised as convenience.

And once the infrastructure is normalized—once CBDCs become the default and cash is phased out—opting out won't be a choice. It will be illegal.

Washington’s digital currency push isn’t just about modernization — it’s about control. But there’s still a way to stay private, independent, and secure.

Discover how to safeguard your IRA or 401(k) with tangible assets like gold and silver — before new policies shrink your financial freedom.

Reagan Gold Group

You won't see the trap close in a single moment. There won't be a dramatic announcement, a switch flipped, a day when freedom ends.

It closes one transaction at a time.

The coffee purchase. The rent payment. The grocery run. Each one logged, analyzed, categorized. Each one feeding a system that knows more about you than you know about yourself.

The infrastructure is built. The pilots are running. The legal frameworks are being drafted. And most people still think it's about making payments faster.

But those watching closely—those who understand that money is power, and control over money is control over life—are moving now. Not in panic, but in preparation. Not rejecting the system entirely, but keeping one foot outside it while the door is still open.

Because once it closes, it won't reopen.

—

Claire West