The Grid Behind the Intelligence

There is a reliable pattern in the history of technological revolutions: the technology that receives the headlines is rarely the technology that becomes the binding constraint.

The steam engine transformed manufacturing. But what ultimately determined the pace of industrialization was the railway network — the miles of track, the iron for rails, the capital for bridges. The internet promised to connect everything. But the pace of the modern digital economy was shaped by fiber-optic cable, submarine lines, and the server farms that made always-on services physically possible. The idea arrives first. The infrastructure catches up slowly, expensively, and on a timeline that rarely matches the urgency of the original vision.

Artificial intelligence is following the same pattern — and the constraint this time is electricity.

Without most people noticing, Elon Musk has started a new venture that has nothing to do with rockets, EVs, Neuralink, or tunnels.

Trump has personally issued emergency support to roll this underlying tech out as fast as possible.

It's already live in multiple states.

Behind the scenes, demand for this is already spiking...

The Financial Times says Sam Altman is begging people on the phone to build this for him and OpenAI.

And the best part for you and your wealth is:

A few little-known companies control the supply chain.

Anyone who wants this tech - be it Sam Altman or even Elon himself - must go through these companies to get it.

You can simply buy their stocks right now... before this news becomes common knowledge.

But you ought to move fast. Because leaked satellite images are already showing up online...

Click here to see how you could back Elon Musk's next venture from your regular brokerage account.

The Invisible Dependency

Every digital service — every search, every stream, every AI query — is ultimately a request for electricity delivered at the right voltage, at the right time, to the right location.

This dependency is usually invisible because, for most of the modern internet era, it was not a meaningful constraint. Power was cheap, abundant, and largely reliable in the markets where digital infrastructure was concentrated. The economic problem in software was always building faster, not powering up.

That assumption is changing. The U.S. Energy Information Administration now projects total U.S. electricity consumption to rise from 4,097 billion kilowatt-hours in 2024 to 4,193 billion in 2025 and 4,283 billion in 2026 — upward revisions driven primarily by data center expansion, with commercial sector electricity use expected to surge 3% in 2025 and 5% in 2026, well above previous forecasts. The electricity system that was designed for a relatively stable demand environment is now absorbing a rapid and uneven load growth that was not part of its long-run planning assumptions.

Why AI Changes the Equation

The energy implications of AI are not simply a larger version of previous computing growth — they represent a qualitative shift in consumption intensity.

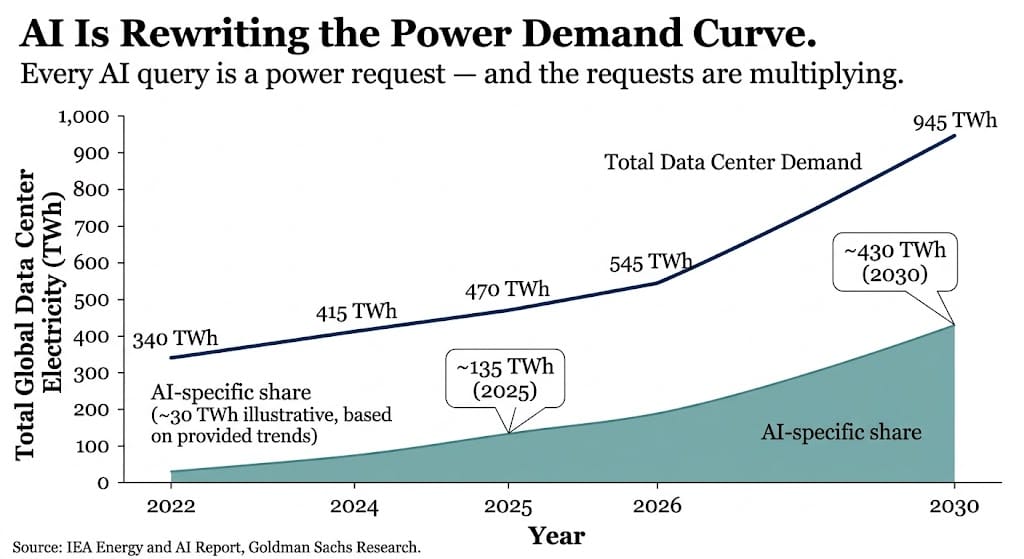

A ChatGPT-class query consumes roughly 0.3 to 3 watt-hours depending on model size and infrastructure, approximately 3 to 10 times the energy of a standard Google search. That difference, multiplied across billions of interactions, compounds quickly. The IEA's 2025 Energy and AI report projected global data center electricity consumption rising from 415 TWh in 2024 to roughly 945 TWh by 2030, with AI accelerator workloads accounting for the largest share of new growth.

Goldman Sachs Research forecasts that global power demand from data centers will increase 50% by 2027 and could rise as much as 165% by the end of the decade compared to 2023. S&P Global's 451 Research calculates that U.S. data center grid-power demand rose 22% in 2025 alone.

Critically, Bloomberg Intelligence analysis suggests efficiency gains from new algorithms and chip architectures are unlikely to reverse this trajectory in the near term: rapid consumer adoption of AI tools may overwhelm any promised reductions in per-unit energy consumption.

Visible Technology vs. Hidden Infrastructure

| What captures attention | What actually enables it |

|---|---|

| New AI model releases and benchmark scores | Grid interconnection approvals, substation capacity, and long-term power contracts morganlewis+1 |

| Hyperscaler announcements and data center leases | Power transformer availability: 30% supply deficit in the U.S. in 2025, lead times of up to 4 years woodmac+1 |

| AI chip performance improvements | Transmission infrastructure: $720 billion in grid upgrades estimated as necessary by 2030 goldmansachs+1 |

| Consumer AI tools reaching millions of users | Cooling systems, water availability, and PUE targets that determine operating cost at scale presenc+1 |

| IPO valuations and venture rounds | Permitting timelines of 3–7 years for new generation and transmission projects about.bnef+1 |

The Bottleneck Economy

Three specific constraints currently bind the pace of AI infrastructure expansion more tightly than compute availability.

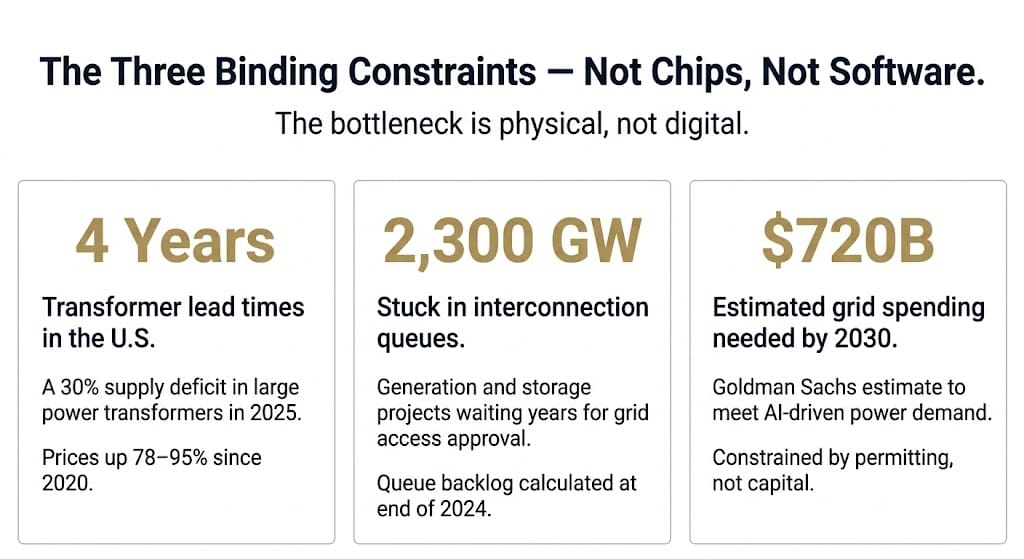

Transformers. Large power transformers are essential to every step of voltage conversion across the grid — more than 90% of all consumed electricity passes through one at some point. Since 2019, U.S. demand for power transformers has surged 116% while domestic manufacturing capacity has failed to keep pace. The result: the U.S. faces an estimated 30% supply deficit in large power transformers in 2025, with lead times extending from a pre-pandemic 30–60 weeks to as long as four years. Prices for distribution transformers are up 78–95% since 2020.

Grid interconnection. Nearly 2,300 gigawatts of generation and storage capacity remained in U.S. interconnection queues at the end of 2024 — projects waiting years for the approvals and infrastructure upgrades required to connect to the transmission network. A DOE analysis warned that absent new firm capacity, blackout frequency could increase by up to 100 times by 2030.

Transmission buildout. Goldman Sachs estimates approximately $720 billion in grid spending through 2030 may be required to meet AI-driven power demand — a figure constrained not by capital availability but by permitting timelines and equipment lead times that "can take several years to permit and build, creating a potential bottleneck for data center expansion." Global grid capital spending rose 16% in 2025 to over $470 billion, its second consecutive year of double-digit growth — and analysts note that even this pace is unlikely to fully eliminate ongoing bottlenecks.

Why Governments Are Paying Attention

Energy infrastructure has moved from a utility concern to a national competitiveness question in the span of roughly two years.

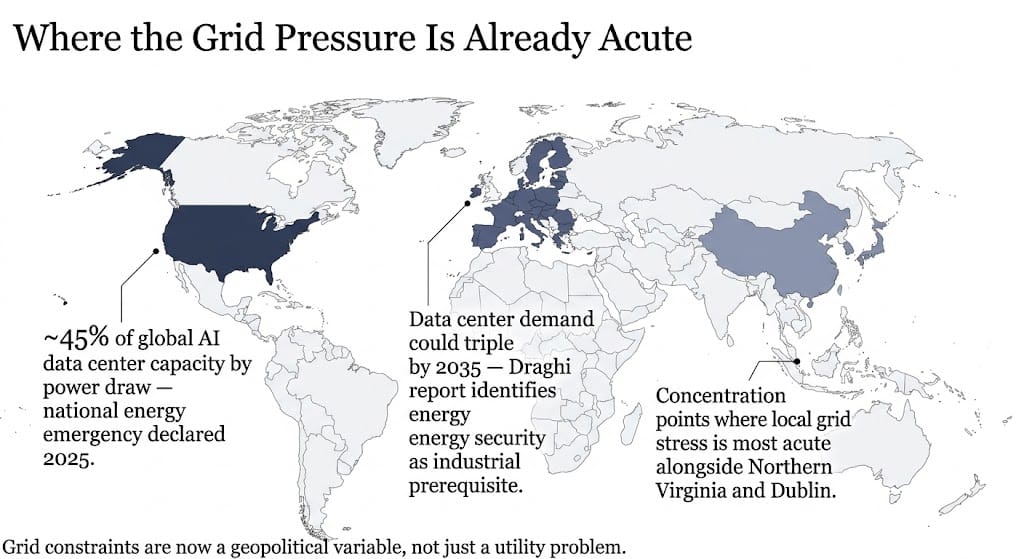

In July 2025, the U.S. Department of Energy published a report on grid reliability and security under an executive order declaring a national energy emergency. The DOE's September 2025 "Speed to Power" initiative explicitly frames grid acceleration as a requirement for "American competitiveness in artificial intelligence." In March 2026, the DOE announced approximately $1.9 billion in funding to accelerate transmission upgrades through the SPARK program.

The European Union faces analogous pressures. A 2026 OECD analysis prepared for the European Commission concluded that data center electricity demand in the EU could rise from 96 TWh in 2024 to 236 TWh by 2035, and that "competitiveness increasingly depends on affordable, always-on electricity." The Draghi report on European competitiveness identified energy security as a structural prerequisite for digital industrial strategy.

The pattern is consistent across geographies: policymakers have concluded that power availability is not a background assumption of the AI economy. It is the AI economy's primary physical constraint.

To avoid 67 million Americans losing power... President Trump is taking drastic action.

Using emergency executive powers, he has paved the way for a new technology 326 times more powerful than the most advanced power generators used by hospitals.

This tech could power the entire country without ever touching oil – and save our crumbling grid from collapse.

It's now also backed by Nvidia CEO Jensen Huang, Elon Musk, and Sam Altman.

But the rights to this tech are cornered by companies most people have never heard of...

And virtually overnight, 3 little-known stocks could soar higher as the public learns how they're involved.

Click here to see the little-known stocks at the heart of Trump's $10 trillion plan for the American power grid.

Risk Lens

The infrastructure opportunity carries distinctive risks that differ from software investing.

Capital intensity and cycle risk. Investor-owned utilities in the U.S. are expected to deploy more than $1.1 trillion across grid and generation infrastructure between 2025 and 2029. This capital is committed over multi-year timelines against demand projections that may shift. If AI adoption curves soften, overcapacity in generation and transmission can persist for decades — the physics of the grid do not unwind quickly.

Regulatory and permitting delays. Transmission permitting in the U.S. can involve multiple federal, state, and local approvals over timelines of three to seven years. Reform efforts have accelerated in some regions but remain fragmented. The OECD analysis of EU regulatory barriers found that in jurisdictions where procedures were not simplified, projects routinely stalled regardless of funding availability.

Technology uncertainty. Efficiency improvements in AI hardware and software are real and ongoing. If new architectures reduce per-query energy consumption faster than adoption grows, demand projections may prove too aggressive, leaving infrastructure built on optimistic assumptions.

Concentration risk. Data center demand is geographically concentrated — the U.S. hosts roughly 45% of global AI data center capacity by power draw, with particularly intense load in Northern Virginia, Singapore, and Ireland. Grid stress in these locations is already acute, creating localized constraints that global investment figures do not fully capture.

The historical record on technological revolutions contains a consistent lesson: the most durable value is often captured not by the technologies that receive the headlines, but by the systems that make those technologies possible.

In the railroad era, the iron mills and the coal that fed them proved essential long after speculative rail ventures failed. In the electrification era, the utilities and equipment manufacturers that wired the country created economic returns that persisted across multiple business cycles. In the internet era, the telecommunications infrastructure built during the late 1990s — much of it through companies that subsequently failed — underpinned the entire subsequent growth of the digital economy.

AI will not be different in this respect. The intelligence is a function of the electricity. The model is downstream of the grid. And the grid is being rebuilt — at a pace, and a cost, and under constraints that may define the shape of the next decade more than any software release.

—

Claire West