The IPO You Imagined Isn't the One That Happened

When Headlines Point One Way, Capital Flows Another

There is a particular kind of story that circulates in personal finance — told at dinner tables, in podcast episodes, in the quiet corners of Reddit threads — about someone who bought shares in a company before the rest of the world noticed. They got in early. The stock multiplied. Their patience was rewarded with life-altering wealth.

These stories are seductive precisely because they feel democratic. They suggest that the market, for all its complexity, still leaves a door open for the ordinary person who pays attention. And in rare cases, that has been true. But the frequency with which these stories are told has very little to do with how often they actually occur — and almost nothing to do with what an IPO is designed to accomplish.

If you've ever felt a rush of excitement watching a company announce its public listing, this piece is meant to slow that feeling down. Not to kill it. Just to introduce it to the machinery behind the curtain.

Imagine living your normal life today... and waking up tomorrow knowing your financial future has shifted.

It happened for early investors in Facebook (a chance to turn $1,000 into $1M)...

It happened in Google (a chance to turn $1,000 into $2.3M)...

And Elon Musk is predicting the SpaceX IPO could be next.

Musk is predicting a 1,000X return for those who position themselves before the July 2026 stampede. He estimates this could turn a tiny $500 stake into $500,000.

The banks are ready. The elites are moving. Jeff Brown’s presentation shows you exactly how to learn to claim a stake for just $500.

Click here to learn how to claim your SpaceX stake for just $500.

The Mythology of Getting In Early

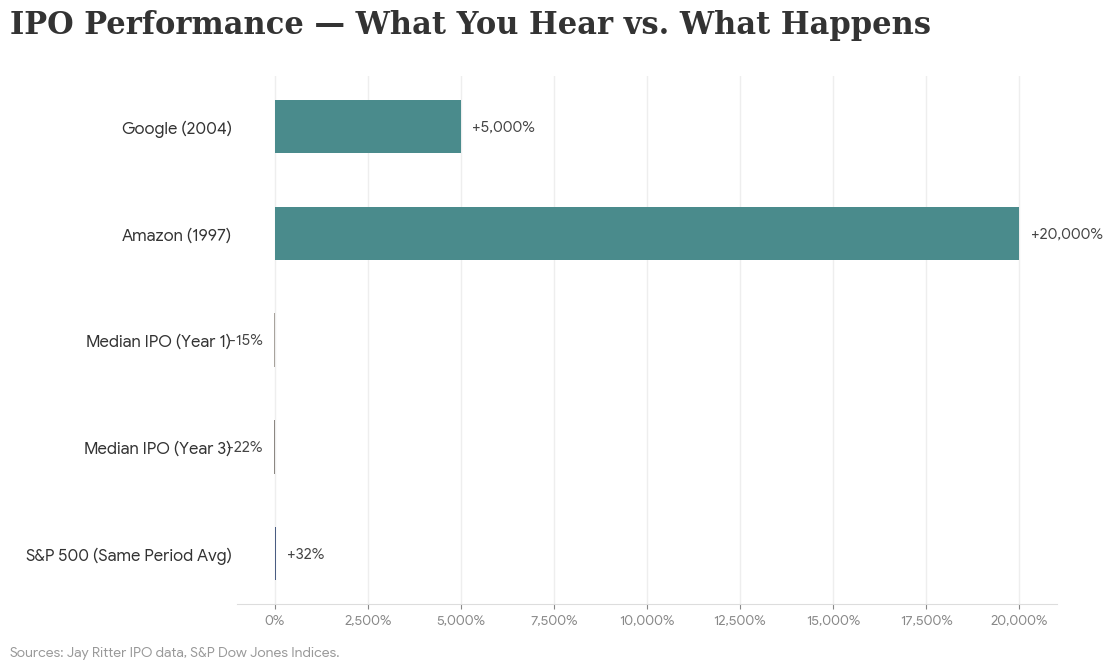

The canonical examples are well known. Google's 2004 IPO priced at $85. Facebook went public in 2012 at $38. Amazon, in 1997, debuted at $18 per share. If you had bought and held, the returns would have been extraordinary — measured not in percentages, but in multiples of your original life.

What is almost never discussed is how many IPOs from the same years produced no such outcome. For every Google, there were dozens of companies that went public, traded sideways for years, diluted their shareholders, and eventually faded from memory. Survivorship bias is not a footnote in this conversation. It is the conversation.

The stories that stick — the ones we retell — are the ones where the outcome was dramatic. But dramatic outcomes are, by definition, statistical outliers. Building an investment framework around them is like designing a retirement plan around lottery odds. The math doesn't work, no matter how compelling the narrative feels.

This does not mean IPOs are irrelevant. It means they are misunderstood.

What an IPO Actually Does

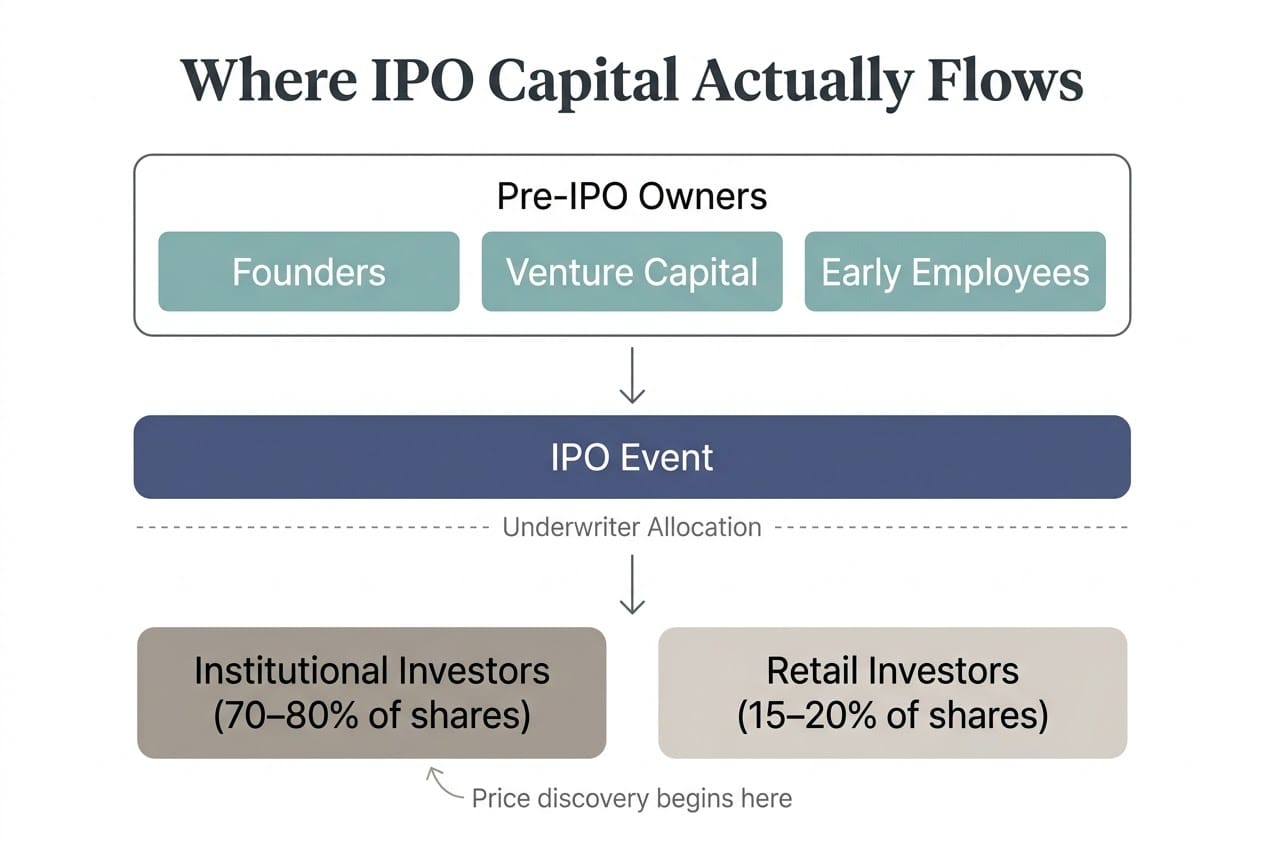

An initial public offering is not, in the most structural sense, an invitation for retail investors to participate in a company's growth. It is a liquidity event — a mechanism through which early investors, founders, and institutional backers convert private equity into publicly tradable shares.

When a company goes public, it is not starting its journey. It is reaching a specific inflection point where the existing ownership structure needs to evolve. Venture capitalists who funded early rounds want an exit. Employees holding stock options want the ability to sell. The company itself may want to raise capital for expansion, reduce debt, or simply establish a public market valuation.

The retail investor enters this picture late. Not because the system is broken, but because that is how the system was designed. Institutional investors — the ones who participate in the IPO allocation process — have relationships, capital commitments, and risk tolerances that give them access to shares before the opening bell. By the time a ticker symbol appears on your brokerage screen, much of the initial repricing has already occurred.

This is not a conspiracy. It is capital structure functioning as intended.

IPO Narrative vs IPO Reality

| What the narrative says | What typically happens |

|---|---|

| "Getting in early" means buying on IPO day | Most repricing occurs in pre-market and first-hour trading |

| IPOs are growth opportunities for retail investors | IPOs are primarily liquidity events for existing shareholders |

| A strong debut signals long-term value | First-day pops often reflect underpricing strategy, not fundamentals |

| Headline returns represent the typical outcome | Median IPO performance trails the broader market within 3 years |

| Retail investors and institutions have equal access | Allocation favors institutional relationships and large capital commitments |

| A well-known brand means a sound investment | Brand recognition and financial soundness are entirely separate variables |

Who Really Gets In Early

Access to IPO shares at the offering price is not distributed evenly. It flows through investment banks, which act as underwriters. These banks allocate shares to their most valuable clients — typically large institutional investors, hedge funds, and high-net-worth individuals who maintain significant brokerage relationships.

Some platforms have begun offering limited IPO access to retail investors, but the volume is small and the conditions are restrictive. You may be able to purchase a handful of shares at the offering price, but the structural advantage still belongs to those who can commit larger sums and absorb greater volatility.

This is not a reason to resent the process. It is a reason to understand it. If you know that the game is shaped by access, timing, and capital scale, you can stop measuring yourself against outcomes that were never available to you in the first place — and start evaluating public companies on their post-IPO fundamentals, where the playing field is more level.

Space Infrastructure: A Category Worth Watching Calmly

One sector where IPO anticipation has been building steadily is space infrastructure — a broad category that includes satellite operators, launch providers, ground station networks, and orbital data platforms.

The excitement is understandable. Space-based infrastructure is becoming foundational to communications, defense, agriculture, and climate monitoring. Some of these companies operate at scales that are genuinely difficult to replicate, and the barriers to entry — regulatory, technical, financial — are enormous.

But this is exactly the kind of category where IPO mythology becomes dangerous. The narrative writes itself: a frontier industry, a handful of dominant players, a sense that getting in early could mirror what happened with early internet companies.

The reality is more measured. Many space infrastructure firms carry significant capital expenditure burdens. Revenue models are often tied to long-term government contracts with uneven payment cycles. The technology is mature enough to function but still early enough to carry meaningful execution risk. And the path from private valuation to public market discovery is rarely smooth.

None of this means the sector lacks merit. It means that evaluating a space infrastructure company requires the same discipline you would apply to a utility or an industrial conglomerate — not the breathless optimism reserved for consumer tech.

The Risk Lens: Dilution, Valuation, and Timing

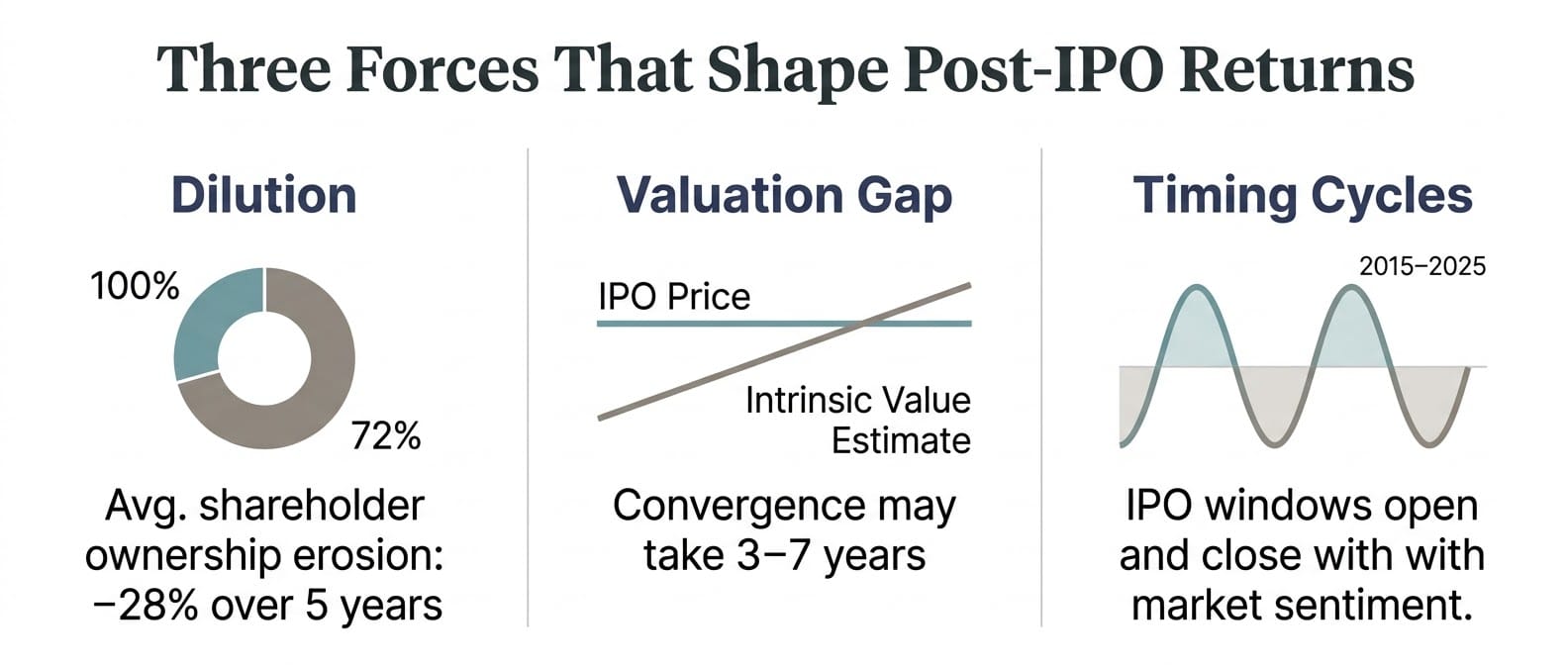

Three forces deserve particular attention when assessing any company in its early public life.

Dilution. Companies that go public often continue issuing shares — to raise additional capital, to compensate employees, to fund acquisitions. Each issuance reduces the ownership percentage of existing shareholders. Over time, dilution can quietly erode returns even when the stock price appears stable.

Valuation. IPO pricing is as much an art as a science. Underwriters aim to set a price that generates first-day demand without leaving excessive money on the table. But the valuation assigned at IPO may bear little relation to the company's intrinsic worth over a five- or ten-year horizon. Paying a premium for enthusiasm is easy. Recognizing that premium in real time is not.

Timing cycles. IPO windows open and close based on broader market conditions, interest rate environments, and investor appetite for risk. A company that goes public during a period of exuberance may enjoy a strong debut but face a harsh correction when sentiment shifts. The timing of your entry matters — not because you should try to time the market, but because you should understand that the market's mood on any given day is not a reflection of a company's long-term trajectory.

Real Wealth Is Built Through Positioning, Not Predictions

The most enduring investment returns rarely come from a single, perfectly timed trade. They come from sustained positioning — from owning shares in structurally sound companies across market cycles, from reinvesting dividends, from resisting the impulse to chase the next transformative listing.

IPOs will continue to generate headlines. Some will deliver impressive returns. But the investor who benefits most is not the one who predicts which ticker will surge on opening day. It is the one who understands what an IPO is, what it isn't, and how to evaluate a company once the confetti has settled.

The door to wealth is not hidden behind a single trade. It is built, slowly, through the accumulation of informed decisions — each one a little less exciting than the story you were told, and a little more likely to work.

—

Claire West