When Scale Looks Unreal, It’s Usually Infrastructure

The largest technological shifts tend to arrive wearing the wrong costume. They look unrealistic at first—too large, too capital-intensive, too far from what a consumer thinks of as “innovation.” They don’t resemble apps. They resemble concrete.

A network diagram can look like science fiction until it becomes a line item. A satellite constellation can look like spectacle until it becomes routing. And an IPO can look like theater until it reveals, quietly, who needs permanent capital—and who is reallocating risk.

This is the part of the cycle that retail investors often misunderstand: the moment when scale stops being a narrative and starts being a balance-sheet problem. That’s where the real structure is built.

The infrastructure thesis

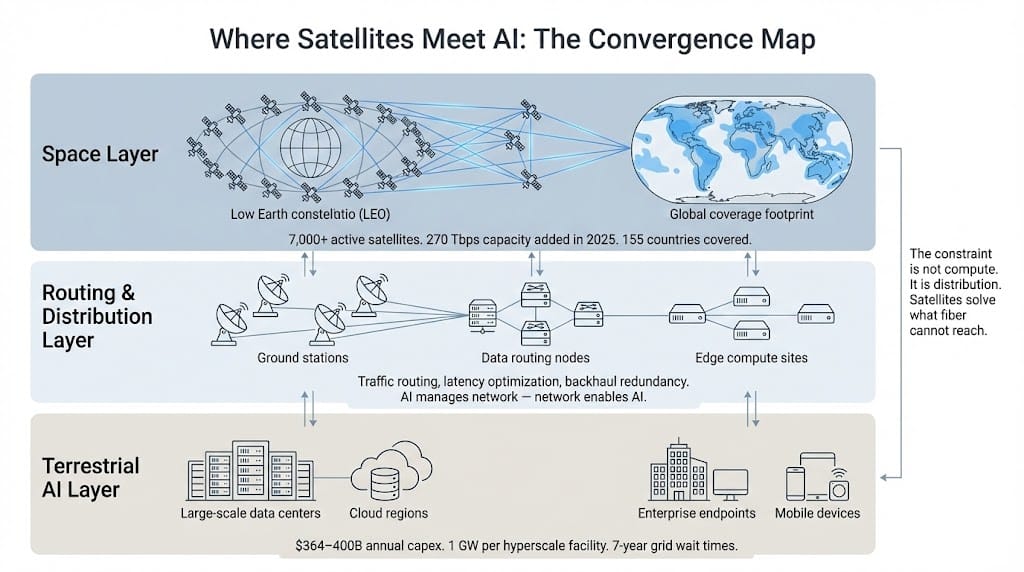

Space infrastructure and AI are converging because both are, at their core, distribution systems. AI distributes intelligence. Satellites distribute connectivity. The overlap is not philosophical—it is mechanical.

AI is increasingly constrained by where data can move, how quickly it can move, and how reliably it can reach the edges of the network where decisions are made. Terrestrial fiber and data centers remain the backbone, but they have choke points: geography, permitting, physical vulnerability, and in some cases political constraints. Low-Earth orbit systems create redundancy and coverage that terrestrial systems cannot match, especially for remote regions, maritime routes, and mobile use cases.

On the technical layer, research on Starlink’s network and LEO performance emphasizes that satellite internet is no longer only “fallback connectivity.” It is measurable infrastructure with its own routing behaviors, performance characteristics, and optimization challenges—exactly the kind of complexity AI systems are built to manage. The convergence is not just that satellites enable AI. It’s that AI increasingly becomes the operating system for satellite networks.

Elon Musk is about to take SpaceX public as part of his plan to unlock the full power of artificial intelligence.

Elon is predicting this will help unleash a $1 quadrillion new wealth wave.

That would be enough to send a check for $2.8 million to every single man, woman, and child in America.

That's how big this opportunity is.

Click here to get the details and I'll show you how to claim your stake… starting with just $500.

Satellites as AI backbone

Starlink is best understood less as a consumer internet product and more as a global routing layer. That framing changes the questions that matter.

Instead of “How many subscribers?” the more structural questions become: How does global traffic move? Where are the bottlenecks? What happens when more devices are always-on, always-connected, and increasingly dependent on cloud inference?

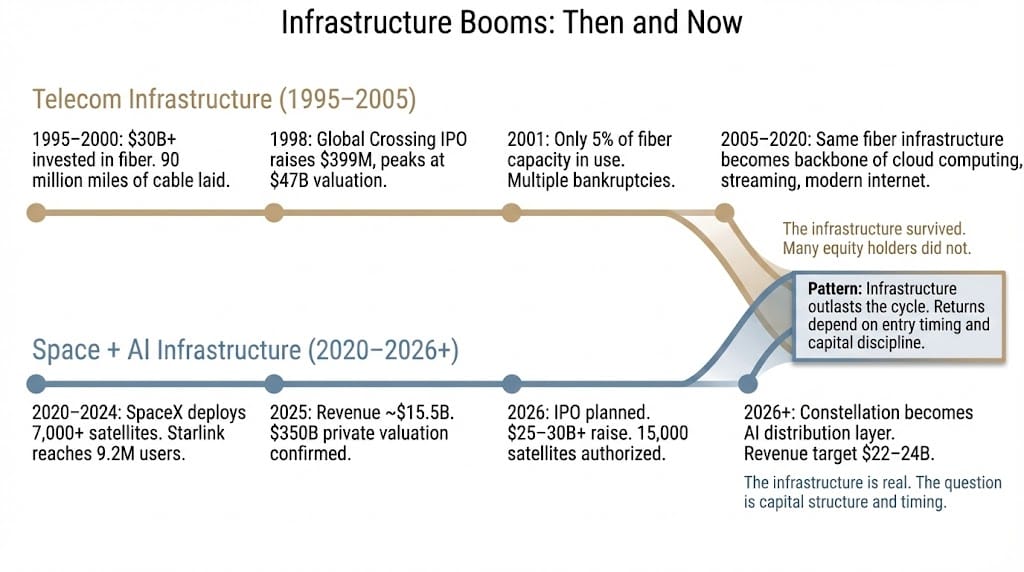

By the end of 2025, Starlink’s user base was reported in the ~9.2 million range by at least one data aggregator, following a rapid ramp from 2021 onward. The same source estimates SpaceX revenue at $15.5B in 2025, with Starlink contributing $10.4B, and notes that many Falcon 9 flights in 2025 were primarily in service of constellation deployment. That is infrastructure behavior: vertical integration feeding a distribution network.

This matters for AI because distribution changes where inference can live. The longer-term direction is not “AI in one cloud region” but AI across many nodes—devices, edge sites, terrestrial data centers, and, increasingly, space-based relays and compute-adjacent architectures. Google Research has explored designs for space-based scalable AI infrastructure, focusing on what it would take to achieve data-center-scale inter-satellite links—tens of terabits per second—using optical networking approaches such as DWDM and spatial multiplexing. Even as these remain early designs, the signal is clear: the conversation is shifting from “connectivity for people” to “connectivity for machines.”

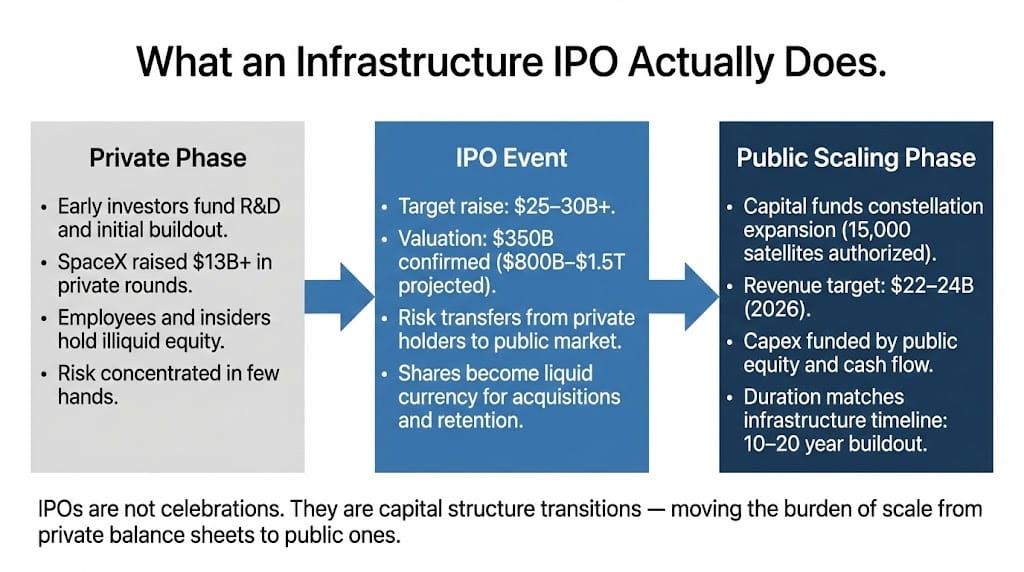

Why IPOs matter structurally

IPOs are often framed as spectacle—bell-ringing, media coverage, retail excitement. Structurally, they are usually about capital formation and risk transfer.

A private company can raise large sums. But public markets offer different advantages: deeper pools of capital, tradable currency for acquisitions, and a liquidity event that allows early investors and employees to rebalance. Importantly, an IPO also changes a company’s time horizon. Infrastructure businesses—satellites, launch cadence, ground stations, data routing layers—tend to be long-duration projects. They are expensive, iterative, and often front-loaded with capital expenditure. Public markets can become the steady funding mechanism that matches that duration.

In December 2025, Reuters reported that SpaceX was pursuing a 2026 IPO and looking to raise above $25 billion, with a valuation over $1 trillion, citing a source familiar with the matter. The same report noted projections of approximately $15 billion revenue in 2025 and $22–$24 billion in 2026, primarily driven by Starlink. Whether those numbers are ultimately realized is less important than what they imply: the market is being asked to finance an infrastructure scaling program, not a single product cycle.

This is why “liquidity events” are rarely just about letting retail participate. They can be about reallocating the burden of scale—moving it from private balance sheets to public ones.

Narrative Scale vs. Economic Mechanism

| Narrative scale (what people hear) | Economic mechanism (what matters) |

|---|---|

| “It’s too big to be real.” | Infrastructure projects are supposed to look unrealistic early; scale is a prerequisite for unit economics in networks. arxiv |

| “The IPO is a payday.” | IPOs are often recapitalizations: extending duration, funding capex, and turning private risk into public equity risk. annualreviews |

| “Satellites are a consumer product.” | Satellite constellations function as routing layers—coverage, redundancy, backhaul, and mobility. ieeexplore.ieee+1 |

| “AI lives in software.” | AI increasingly lives in systems: compute placement, network performance, energy, and uptime constraints. arxiv |

| “Astronomical projections prove inevitability.” | Extreme numbers often reflect optionality, not certainty; they can obscure execution risk and capital intensity. finance.yahoo+1 |

| “Retail wins by buying the headline.” | Early beneficiaries are often infrastructure owners and intermediaries who finance, build, and operate the rails. annualreviews |

The psychology of astronomical numbers

Large numbers trigger the wrong mental models. They pull people toward lottery math.

When valuations are discussed in trillion-dollar terms, or subscriber counts are projected decades forward, the mind reaches for inevitability. It starts treating scale as destiny rather than as a cost structure. This is where retail narratives become least reliable: they confuse the possibility of scale with the mechanics of building it.

Bloomberg coverage in December 2025 framed an “audacious” $1.5 trillion valuation target for a potential SpaceX listing, describing revenue forecasts of $22–$24 billion in 2026, largely fueled by Starlink. That framing is instructive because it highlights the tension: the story can be told as vision, but the valuation ultimately rests on throughput—revenue, margins, capex discipline, and execution pace.

Astronomical numbers distort rational thinking in two directions:

- They create premature dismissal (“it’s absurd”), causing investors to ignore real infrastructure signals.

- Or they create premature belief (“it’s inevitable”), causing investors to ignore execution risk and capital structure.

Neither response is analytical. The correct response is slower: map incentives, map funding needs, map bottlenecks.

Historical parallel: telecom IPO cycle

The late 1990s telecom boom is a useful mirror because it was also an infrastructure sprint justified by demand narratives.

Companies raised capital rapidly to lay fiber and build global networks. IPOs arrived early in corporate life cycles. In some cases, there was genuine long-term value in the infrastructure built—even when the companies themselves failed. CNN once summarized the era as firms plowing roughly $30 billion into the ground, building 90 million miles of fiber-optic cable; by 2001, an estimate suggested only 5% of fiber capacity was being used. The crash was real, but so was the backbone that later enabled the modern internet economy.

A separate retrospective noted that Global Crossing went public in 1998, raising $399 million in its IPO and reaching a peak valuation near $47 billion—before later collapsing into bankruptcy. The arc matters because it shows how IPOs can fund infrastructure buildouts that overshoot near-term demand, creating both overcapacity and long-run option value.

That is the cautionary parallel for space infrastructure tied to AI distribution: it can be strategically necessary and still financially mistimed. Retail investors often confuse these.

Some analysts believe a potential public listing tied to next-generation satellite infrastructure could reshape how AI systems are distributed globally. A recent briefing outlines the structural logic behind this thesis and how smaller investors evaluate participation.

Risk lens

Infrastructure-scale bets rarely fail because the story was wrong. They fail because timing, financing, and coordination are unforgiving.

Key risks that deserve sober attention:

- Capital intensity and dilution risk: Public markets can fund scale, but they can also reprice risk abruptly if buildout costs rise faster than revenue. The point isn’t that an IPO “means upside.” It means a new capital structure with new pressures.

- Regulatory and spectrum constraints: Constellations operate under licensing and coordination regimes. Changes in approvals or compliance requirements can slow deployment and alter economics.

- Technical limits and network complexity: Performance variability, routing behavior, congestion management, and ground station dependency are not marketing details; they are operational realities measured in ongoing research.

- Overbuild and demand mismatch: The telecom era shows how quickly optimism can finance excess capacity. Overcapacity can still be useful later, but equity holders may not be paid for patience.

- Narrative fragility: When the story relies on extreme future adoption, sentiment can swing faster than infrastructure can adjust—because infrastructure is slow.

Risk here is not a reason for fear. It’s a reason for literacy.

Elon Musk is predicting it will unleash $1 quadrillion in new wealth and give investors

who get in today a chance to turn each $100 invested into $100,000.

Brownstone Research

Space infrastructure and AI converge not because the future is glamorous, but because the present is constrained. Distribution becomes destiny when compute and data are everywhere, and connectivity is the silent condition for both.

IPOs, in that context, are rarely fireworks. They are financing events—strategic reallocations of who funds the buildout and who holds the risk. Retail investors tend to read them as spectacles. Institutional actors read them as plumbing.

Scale is built through capital discipline, not slogans. The most durable advantages in technology cycles come from owning the rails—routing, bandwidth, latency, redundancy—not from repeating the biggest number on the slide. And the first signs of that shift almost always look unrealistic, right up until they become infrastructure.

—

Claire West