The Door That Feels Like It's Opening

You are reading through a regulatory filing — dense, bureaucratic, written in the language of lawyers and accountants. Then a name appears. A private company, mentioned in a disclosure. A company you have heard described in terms of transformative growth, exclusive investors, and a trajectory that sounds like every legendary startup story you have ever read.

Something shifts in the reading. The document feels less like a legal text and more like an invitation. A door, slightly open. A chance to be early.

That feeling is worth examining carefully. Not because it is wrong, but because it is almost perfectly designed to bypass the questions that matter most.

The Mythology of Getting In Early

The story of early-stage investing is largely a story about a few spectacular outcomes told repeatedly, stripped of their context.

The early Facebook investors who turned small stakes into enormous returns. The Google angel investors. The people who held Nvidia through the years when it looked like a niche chip company. These stories are accurate. They are also the visible peak of a distribution that includes thousands of private investments that never went public, never returned capital, or returned it modestly after many years of illiquidity.

This is survivorship bias in its purest form: the mind calibrates expectations on the outcomes it can see, which are systematically selected for success. The venture capital data is instructive. NBER research on venture capital returns documents a distribution that is highly right-skewed — a small number of investments generate most of the returns, while the majority underperform or fail entirely. The investors who achieved the legendary outcomes had typically done dozens of investments; the per-investment failure rate was high even in the best portfolios.

What retail investors encounter when they hear early-stage stories is not the full distribution. It is the tail.

Why Private Markets Changed

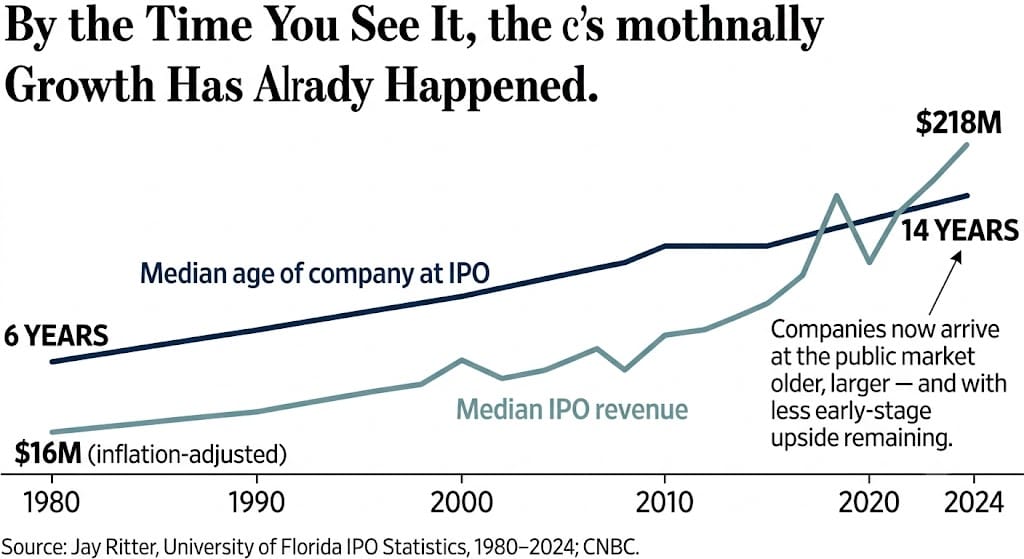

The context for pre-IPO excitement has a structural explanation that is worth understanding in precise terms.

In 2000, the median age of a venture-backed company at its IPO was approximately 6 years. By 2024, that median had risen to 14 years. The number of VC-backed companies going public fell from 245 in 2000 to just 37 in 2024. The companies that did go public in 2024 had median revenues of $218 million — up from $16 million in 1980, adjusted for inflation.

The reason is structural, not coincidental. Private capital is now abundant at a scale that was simply unavailable two decades ago. Databricks raised $10 billion in a single private round in December 2024. OpenAI raised $6.6 billion in October. SpaceX raised $1.25 billion. Global private equity assets under management now exceed $12 trillion, projected to grow to $25 trillion by 2030. Companies no longer need public markets to fund growth. They go public — if they go public at all — for different reasons and at a much later stage.

The consequence for public investors is significant: the period of highest growth — the years of compounding from early product-market fit through scale — is increasingly captured entirely within private markets. By the time a company lists, institutional and private investors have often already participated in the most dramatic valuation step-ups.

The Access Gap

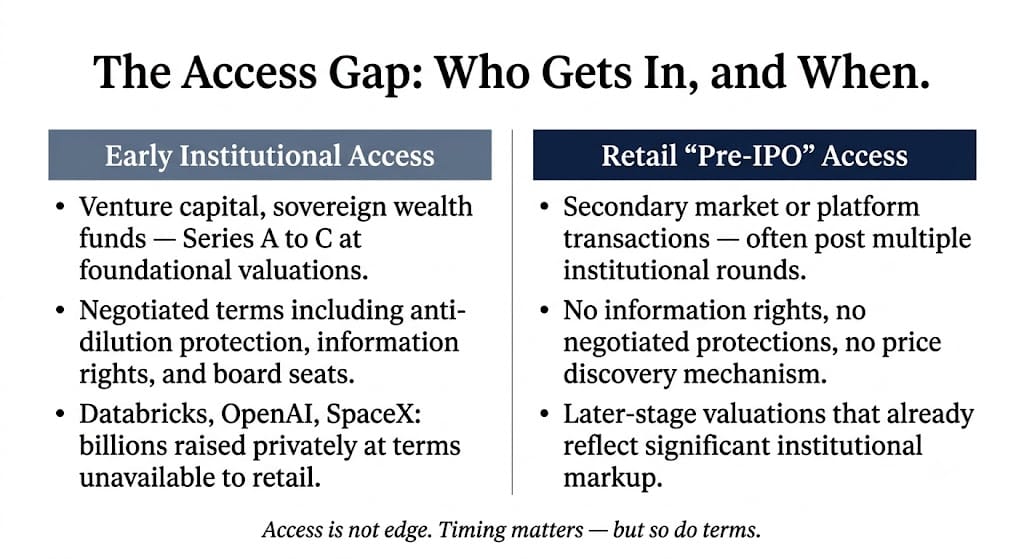

Pre-IPO access is not a level playing field, and the mechanics of who gets in first are worth understanding.

Institutional investors — venture capital firms, sovereign wealth funds, growth equity funds — receive first call on early rounds, typically at valuations that bear no resemblance to the late-stage prices retail investors might encounter. Accredited investors under SEC Regulation D must meet financial thresholds: net worth above $1 million excluding primary residence, or annual income above $200,000. Even within this group, meaningful early-stage access depends heavily on relationships, track record, and geographic proximity to deal flow.

What retail investors typically encounter — through platforms, funds, or informal secondary market access — is not the same as what early institutional participants receive. It is later-stage exposure, often in secondary transactions, at valuations that already reflect significant markup from the original investment rounds.

Pre-IPO Narrative vs. Investment Reality

| Dimension | The narrative | The reality |

|---|---|---|

| Emotional appeal | "Get in before Wall Street" — exclusivity, timing advantage jarsy | Most retail access arrives after multiple institutional rounds have already captured early growth williamblair |

| Liquidity | Private shares imply eventual IPO exit | No guaranteed liquidity event; IPO may be delayed years or never occur; lock-up periods apply post-listing linkedin+1 |

| Valuation transparency | Assumes price reflects fair value | Private valuations are set in negotiated rounds; public comparables may not apply; no continuous price discovery linkedin |

| Access mechanics | Feels like an open door | Structured by regulation, accreditation, and relationships; retail access is typically late-stage and secondary jarsy+1 |

| Risk profile | Implies contained downside due to company reputation | Concentrated, illiquid, with limited information rights; fraud risk in informal secondary markets linkedin |

| Upside narrative | Built on visible winners; implies repeatability | VC return distribution is highly skewed; most investments do not produce outlier returns papers.ssrn+1 |

Why Celebrity Proximity Works

The attachment of well-known names to private investment narratives is not accidental. It follows a documented behavioral pattern: the halo effect.

Research on the halo effect in investing finds that an admired individual — a charismatic CEO, a legendary investor — creates positive evaluative coloring that extends well beyond what the person's specific involvement justifies. When a famous name is associated with a company or investment, investors tend to transfer their trust in the person to the underlying asset, often without separately evaluating whether the association is meaningful, what terms the famous investor received, or whether those terms resemble the ones now being offered.

A 2024 study on investor psychology found that 71% of retail investors are more likely to purchase an asset if endorsed by a celebrity. The mechanism is not logic — it is social proof and trust transfer. Famous people signal legitimacy. Legitimacy reduces the felt need for due diligence. Reduced due diligence increases vulnerability to the exact risks that due diligence would surface.

The relationship between a famous name and a private company can be meaningful — or it can be adjacent, historical, or purely promotional. Separating those possibilities requires asking specific questions the narrative is not designed to encourage.

What Ordinary Investors Should Actually Ask

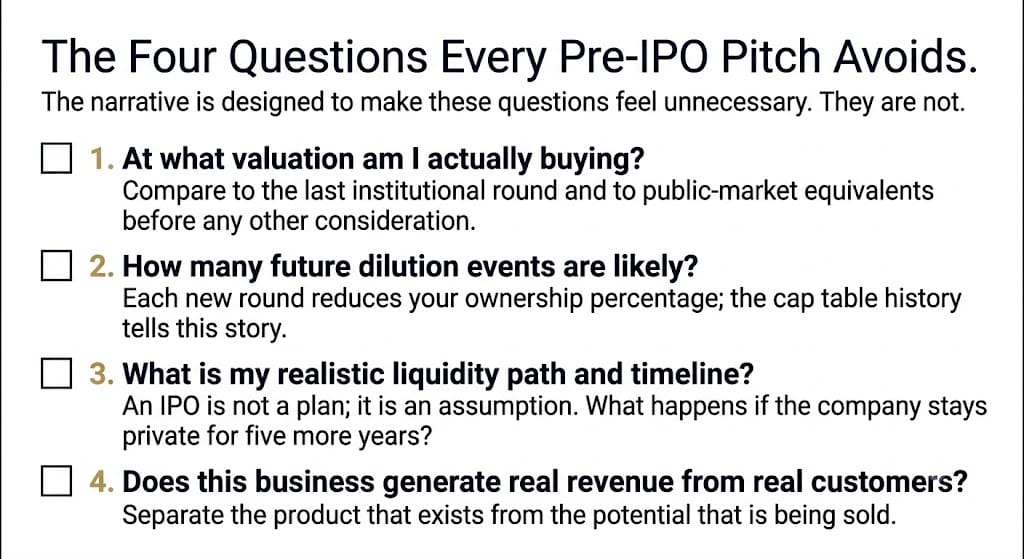

If you are considering exposure to any private company — through a fund, platform, secondary market, or direct offer — these are the questions that matter, before any other consideration:

Valuation. At what price am I buying? How does that compare to the last institutional round? What multiple of revenue or earnings does it imply, and how does that compare to public-market equivalents?

Dilution. How many more funding rounds might occur before a liquidity event? Each new round typically dilutes existing shareholders. The cap table history reveals how aggressively the company has issued new equity.

Liquidity path. When, specifically, might I be able to sell? Is an IPO actually planned, or assumed? What happens to my investment if the company is acquired, stays private indefinitely, or raises a down round?

Revenue quality. Is the business generating real revenue from real customers paying real prices? What is the unit economics story — customer acquisition cost, retention, gross margin?

Business model. Does the company have a product that exists, customers who pay for it, and a clear path to profitability? Or is the value proposition primarily about future potential?

Editor’s Note: Former tech executive Jeff Brown picked Bitcoin, Tesla, and Nvidia before they jumped as high as 52,400%, 2,150% and 36,000%. Now he’s recommending an Elon Musk-backed startup that has been called “the fastest-growing business in the history of capitalism.” And you can claim your pre-IPO stake for less than $50. Click here to see the details and get the name of this startup, 100% free… or read more below.

See this document below?

Elon Musk just revealed what I believe is the biggest investment opportunity of the year when he filed this official document with the SEC.

Because on page 146 he revealed the name of a startup that’s set to be…

The next monster IPO on Wall Street. (Click here to get the details.)

Even though this has nothing to do with robots, self-driving cars, or rockets…

This startup is growing faster than Tesla…

Faster than SpaceX…

And it’s even growing 23 times faster than Nvidia.

That’s why The Atlantic called it…

“The fastest-growing business in the history of capitalism.”

These types of explosive IPO opportunities are normally off-limits to everyday folks like you.

They’re reserved for rich people on Wall Street and Silicon Valley.

But I found a way for you to claim your stake before the IPO… starting for less than $50.

Click here to see the details, including the name of this startup, completly free of charge.

Risk Lens

Access is not edge. This is the distinction that the pre-IPO narrative most consistently obscures.

The question "can I get in?" and the question "should I get in, at this price, with this information, at this stage?" are different questions. Platforms and intermediaries that lower minimum investment sizes have made the first question easier to answer affirmatively. They have not changed anything about the second.

Small minimum investments do not reduce concentration risk — they reduce the dollar amount at risk while preserving all of the structural disadvantages: limited information, illiquidity, valuation opacity, dilution exposure, and the absence of the protections that accredited and institutional investors typically negotiate.

Regulatory bodies including the SEC and SEBI have separately issued warnings about fraud and misrepresentation in informal pre-IPO secondary markets. The combination of retail enthusiasm, limited regulatory oversight, and informal transaction structures creates conditions that attract bad actors.

The most important question in pre-IPO investing is not whether you can get in early. It is whether you understand what you are actually buying — at what price, under what terms, with what realistic liquidity expectations, and on what evidence.

The feeling of an opening door is powerful precisely because it is rare. Rarity triggers urgency. Urgency is the enemy of the analysis that any investment of this type requires.

The companies that have built durable value have mostly done so over long periods, with unglamorous consistency, in conditions that looked unremarkable at the time. The mythology around early access is built on the exceptions — not the pattern.

Understanding the difference between the two is where clarity begins.

—

Claire West