The Quiet Lie of a Crowded Chart

Don't download my free "Simple Options Trading For Beginners" book if:

❌ You enjoy spending 8 hours a day staring at charts

❌ You think trading should be complicated to be profitable

❌ You like the adrenaline rush of risking your retirement on one trade

❌ You believe the "experts" who say you need to master 50 strategiesBut if you're tired of all that...

If you'd rather spend 10 minutes a night on your trades and the rest of your time actually living your life...

Then this free book might be the most important thing you read this year.

It contains the exact techniques I stumbled onto after losing a small fortune trying everything else.

The same techniques that now let me trade from my summer home in Michigan (or my winter home in Florida), spend afternoons with my family, and sleep peacefully at night.

You'll discover:

- The "boring" technique that consistently outperforms complex strategies.

- Why most options education actually makes you a worse trader.

- How to know within 10 minutes if a trade is worth taking.

It normally sells for $29.97, but right now it's free.

Get your copy here (if you actually want simpler trading).

P.S. Once I switch this back to $29.97, that's where it stays.

Download your free copy here before that happens.

A Late Night That Looks Like Work

It is midnight, and the screen is full of information.

Three charts are open. A moving average study in blue. A momentum oscillator at the bottom. A volume histogram on the side. There is a watchlist with twelve symbols, each flagged with a different indicator. A second tab holds a screener with eleven filters applied. A third holds a forum thread where someone has posted a trade idea that uses a strategy you have not fully read yet.

This feels, in the moment, like diligence. It looks like the visual language of expertise. But the position you are watching has not changed, your analysis has not become more accurate, and somewhere in the accumulation of inputs, the actual decision has become harder to make — not easier.

This is the core tension in modern financial self-education: the tools designed to help have become a form of performance. Complexity has become a substitute for clarity, and the two are not the same thing.

Why Complexity Feels Intelligent

The preference for complicated financial systems is not irrational — it follows from a coherent, if misleading, set of intuitions.

Research Affiliates, in their analysis of the investor bias toward complexity, describe the mechanism precisely: when presented with a complicated strategy, investors engage first in automatic, associative thinking — "I don't understand this, so it must be sophisticated" — which then becomes a basis for trust. The complexity of the system signals that someone, somewhere, has done the hard thinking. The investor defers to that implied intelligence.

This bias is reinforced structurally. Asset managers who charge higher fees need justifications for those fees — and complexity provides one. Consultants who recommend managers benefit from systems that require interpretation. Financial media generates engagement through novelty and action, not through the dull discipline of waiting. The entire architecture of financial information delivery rewards the appearance of analysis over the discipline of restraint.

The result is an environment where dashboards with more indicators feel more professional, more subscriptions feel more informed, and more activity feels more productive — regardless of whether any of it improves outcomes.

The Psychology of "More"

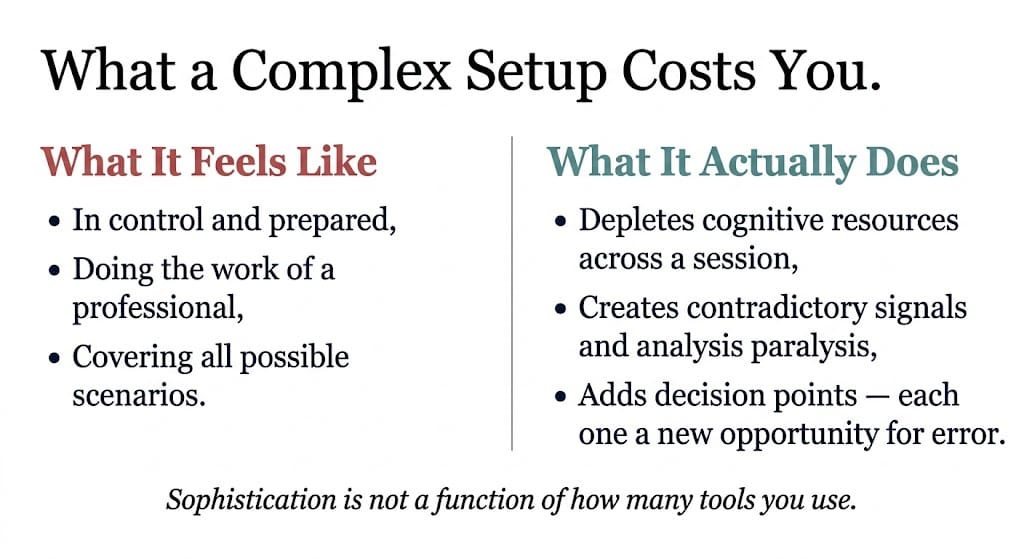

The problem with adding indicators is not that they contain no information. It is that adding more of them does not compound insight — it compounds noise, decision points, and the opportunity for contradiction.

As trading frequency increases, the quality of individual decisions tends to decline. Decision-making requires attention, analysis, and evaluation — resources that deplete across a session. Research on cognitive load and investment decisions finds that under mental strain, risk-taking increases and analytical rigor decreases — the opposite of what most investors intend when they add more tools to their setup.

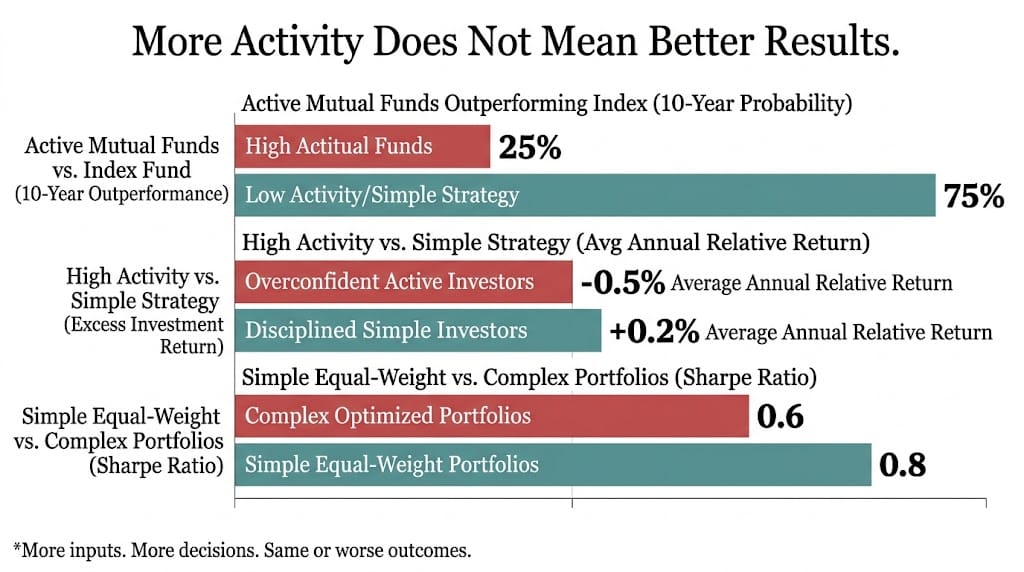

Overconfident investors, who tend to believe their additional analysis is generating additional edge, trade approximately 30% more often than the average investor, according to behavioral finance research — and the excess trading does not produce excess returns. In 2023, only about 25% of actively managed mutual funds outperformed the market over the previous ten years. The professionals with access to the most sophisticated systems, the deepest data, and the most indicators failed to beat a simple index fund three-quarters of the time.

The additional layer of tools did not explain that failure. In many cases, it contributed to it.

Complexity Signal vs. Actual Value

| Complexity signal | Actual value delivered |

|---|---|

| Five or more indicators on a single chart | Overlapping, often contradictory signals; increased decision fatigue without improved prediction globalbankingandfinance+1 |

| Multiple active strategies running simultaneously | Exposure to conflicting rules; difficulty attributing outcomes to any single approach researchaffiliates |

| Constant monitoring of an open position | Emotional volatility from noise; tendency toward premature exits driven by short-term movement globalbankingandfinance+1 |

| Frequent strategy switching based on recent performance | Performance chasing; entering strategies after their peak effectiveness researchaffiliates+1 |

| High subscription count to financial newsletters | Information overload; confirmation bias amplified by volume of inputs activtrades+1 |

| Sophisticated portfolio optimization models (retail) | Research finds simple equal-weighted strategies consistently match or outperform complex optimization in Sharpe ratio and turnover at retail level etd.ceu |

Why Simple Systems Are Emotionally Harder

Here is the part that complicates the case for simplicity: it is not psychologically easier. In many ways, it is harder.

A simple system generates fewer signals. Fewer signals mean fewer actions. Fewer actions mean longer periods of waiting — and waiting feels unproductive in an environment designed to generate the feeling of productivity. When a simple rule says "do nothing," every piece of incoming information becomes a test of discipline rather than an invitation to engage.

Simplicity also eliminates plausible deniability. When a complex strategy produces a loss, there are many potential explanations: a filter that should have been tuned differently, an indicator weight that was miscalibrated, a signal that came too early. The complexity diffuses accountability. A simple rule — "buy when X, exit when Y" — makes the failure legible and personal.

There is also the matter of social context. A person who describes their process as "I watch one thing and wait" is not a compelling conversationalist in spaces where sophistication is performed. The socially legible identity is the one with the screener, the multi-screen setup, the proprietary watchlist.

These are not trivial pressures. They are the psychological environment in which most individual investors operate.

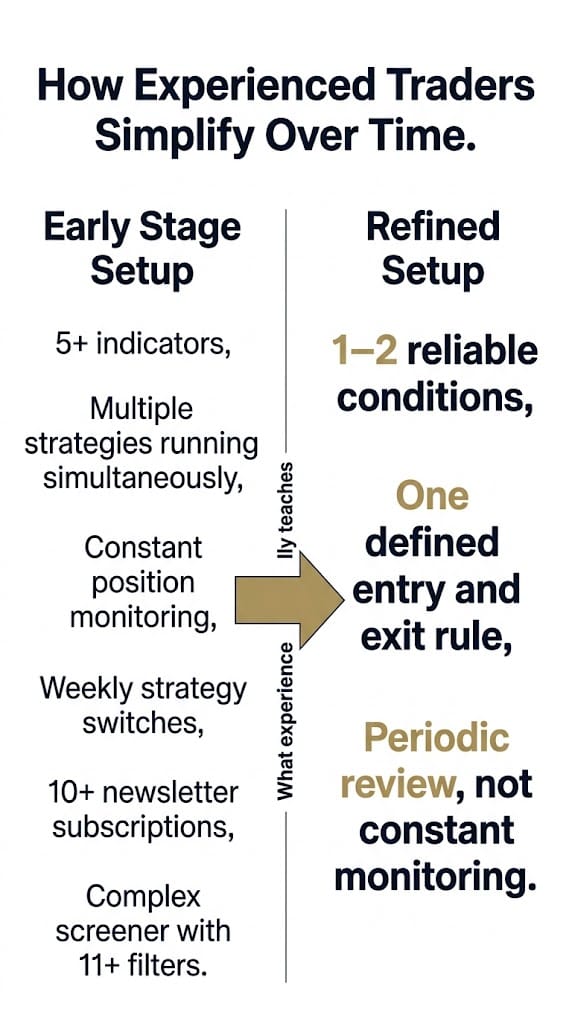

How Professionals Reduce, Not Add

The pattern among experienced traders and portfolio managers who perform consistently is not the addition of variables — it is the removal of them.

Former hedge fund managers who have written about their transitions frequently describe the realization that their edge, such as it was, came from a small number of reliable conditions — and that the surrounding complexity was adding cost and noise, not return. A CFA charterholder in a documented discussion on complexity versus simplicity noted that "every additional fund, strategy, or rule adds another decision point, and every decision point is another opportunity for behavioral error."

Systematic strategies work by defining rules precisely and following them mechanically — not because mechanical rules are smarter than human judgment, but because they remove the continuous decision-making that depletes cognitive resources and introduces emotional volatility. The discipline is not in the system's complexity. It is in the commitment to not override the system.

FREE: Discover The Safer & Simpler Way to Start Trading Options

Profits Run

Risk Lens

Simplicity is not a risk management strategy. It is a decision-making posture — and the two are not the same.

A simple system with poor risk parameters is still a high-risk system. Fewer indicators do not protect against inappropriate position sizing, undiversified exposure, or the absence of a defined exit condition. The argument against unnecessary complexity is not an argument for complacency. It is an argument for clarity about what your system is actually doing, how much you are risking, and why.

There is also the risk of mistaking simplicity for passivity. Reducing the number of inputs requires ongoing judgment about which inputs actually matter — a form of active, disciplined curation that is harder than it appears. The investor who has removed everything except one indicator has to be confident they have removed the right things, and has to resist adding them back when the market produces a period of unclear signals.

Finally, simpler systems are easier to backtest — but backtesting has its own pitfalls. A rule that performs well historically may have been generated by conditions that no longer exist. Simplicity does not solve the problem of overfitting to the past.

The goal of a financial system is not to keep you engaged. It is not to signal your seriousness. It is not to give you something to do during periods of uncertainty.

The goal is to make better decisions, less often, with less friction and less emotional interference. Those objectives are not served by more data, more subscriptions, or more screens. They are served by understanding what you are actually trying to do, designing the simplest system that does it, and developing enough discipline to follow it when everything around you is suggesting you do something else.

Clarity is harder to achieve than complexity. It is also the only thing that tends to work.

—

Claire West