The Lien Behind the Property

Have you checked out the tax lien list from your state?

There’s literally thousands of houses investors earn monthly income from...

-- without dealing with rentals

-- without costly marketing

-- without cold-calling

And get this...

The returns are 100% backed by the government.

No kidding.

Can you imagine the government paying us for once?

Rather than the other way around.

Access the Tax Lien List

A List on a County Website

Somewhere in the public records of almost every American county is a list. It catalogs properties with unpaid taxes — addresses, parcel numbers, amounts owed. The list is public by design, part of the mechanism that allows local governments to collect revenue they are legally owed.

Some investors find this list and see opportunity. The logic has surface appeal: the government wants its taxes paid; investors can pay them; the law sets the terms of repayment with interest. It sounds structured, backed by real property, less speculative than the stock market. Depending on where you are reading this, you may have encountered a version of this idea described as "passive income guaranteed by the government."

That framing deserves scrutiny. Tax lien investing is a legitimate, structured strategy — but it is not what the most enthusiastic descriptions suggest. Understanding the mechanism precisely is more useful than either the promotional version or reflexive dismissal.

What a Tax Lien Actually Is

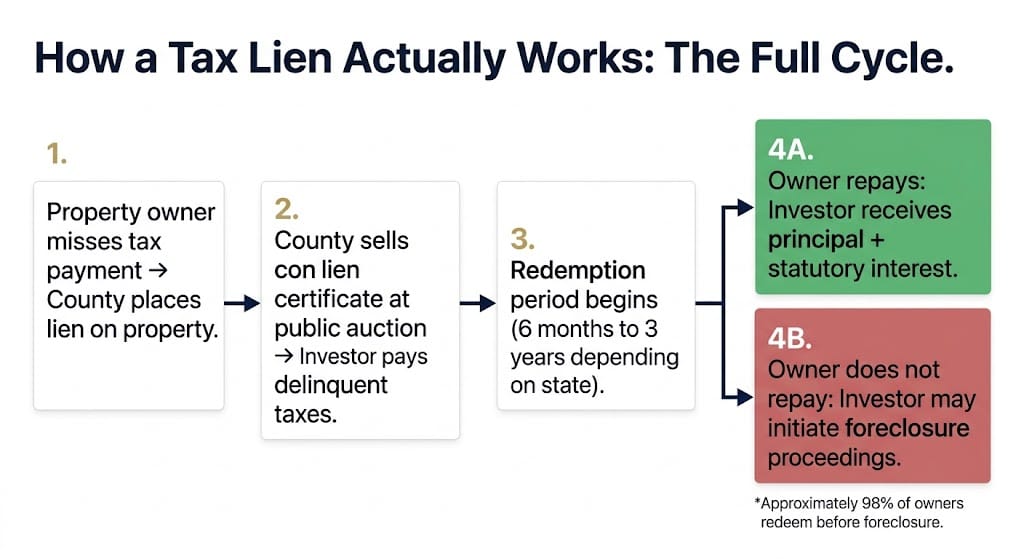

When a property owner fails to pay property taxes, the local government places a lien against the property — a legal claim that must be satisfied before the property can be sold with clear title. In approximately 29 states, plus the District of Columbia, the government then sells that lien at public auction to investors. The government receives its unpaid taxes immediately; the investor receives a certificate representing the legal right to collect what is owed, plus statutory interest, from the property owner.

This is a legal claim — not ownership. The investor does not acquire the property at the auction. They acquire a structured instrument secured by the property, with the right to begin foreclosure proceedings if the debt is not repaid within a defined redemption period.

That distinction carries practical weight. Owning a tax lien certificate means owning a time-limited, legally specific claim against a specific parcel of real estate. What happens next depends on the property owner, state law, property condition, and a range of factors the investor cannot fully control at the moment of purchase.

How Investors Make Money

The return mechanism is straightforward in structure, if variable in outcome.

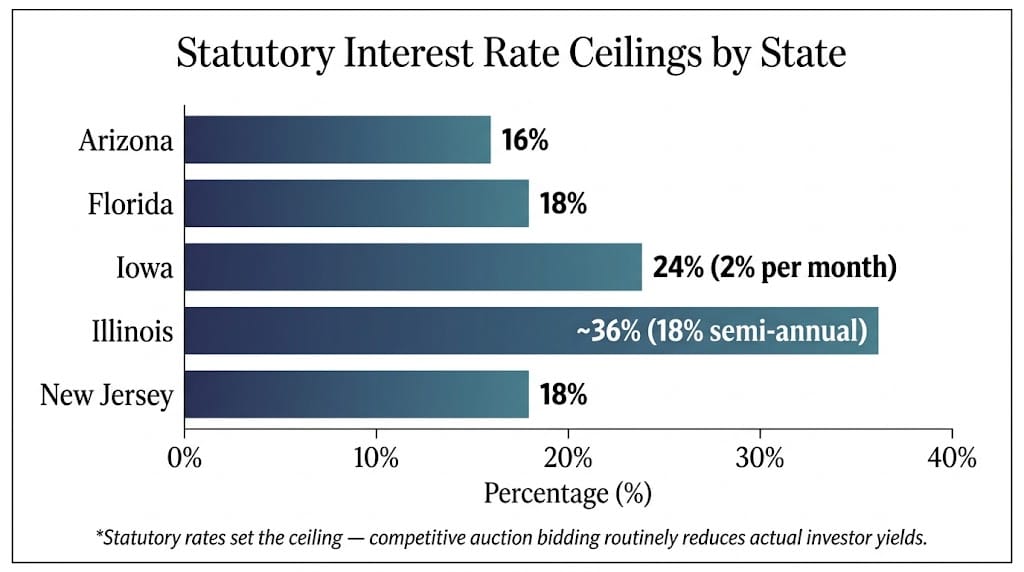

If the property owner repays the delinquent taxes within the redemption period — which typically runs six months to three years depending on the state — the investor receives their principal back plus statutory interest. Interest rates vary significantly: Arizona caps at 16% annually; Florida at 18%; Illinois charges 18% twice per year for an effective rate near 36%; Iowa charges 2% per month. In competitive auction markets using a bid-down method, investors often accept rates well below the statutory maximum in order to win the certificate.

If the owner does not repay within the redemption period, the investor may have the right to initiate foreclosure and potentially acquire the property. In practice, approximately 98% of property owners redeem their liens before foreclosure — meaning most investors profit from interest income, not property acquisition.

The national tax lien market grew from $3.8 billion in 2021 to $5.02 billion in 2024, with both parcel counts and total dollars rising. That growth reflects both increased investor interest and higher underlying property valuations driving up lien amounts.

Tax Lien Myth vs. Reality

| Common claim | Structural reality |

|---|---|

| "Backed by the government" | Backed by a specific parcel of real estate, not by a government guarantee; the property is the collateral freedommortgage+1 |

| "Guaranteed interest rates up to 36%" | Statutory rates set a ceiling; competitive auctions routinely bid rates down; actual yield depends on timing and competition coretaxdeeds+1 |

| "You own the property if they don't pay" | You gain the right to begin foreclosure proceedings — a legal process with costs, timelines, and no guarantee of clean title taxliencode+1 |

| "Passive income" | Requires active due diligence per property, ongoing monitoring of the redemption period, and legal action if unredeemed financialmodelslab+1 |

| "Safe because it's real estate" | Property may be vacant, contaminated, condemned, or hold less value than the lien amount midatlanticira+1 |

| "Available to any investor" | Institutional investors — banks, hedge funds, and dedicated lien funds — dominate many large-market auctions rocketmortgage |

The Appeal

The structural features that attract investors to tax liens are real, not invented. The interest rates are set by state law, not market negotiation — creating a defined ceiling on what you can earn if the lien redeems. The investment is secured by real property, not an unsecured promise. The legal framework is codified and public, which makes the rules knowable in advance.

For investors who are frustrated by the opacity of financial markets, this has genuine appeal: here is a process, governed by statute, with a defined outcome path. That combination of legal structure and property backing creates a perception of solidity that equity or bond investments often lack.

The perception is partially accurate. The structure is real. The problems arise when that structure is treated as equivalent to a guarantee.

The Overlooked Risks

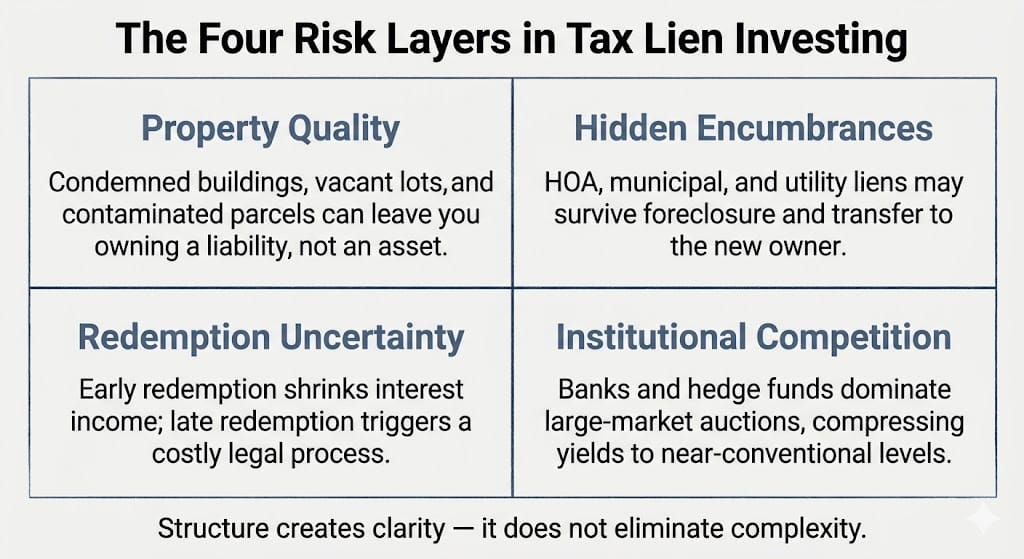

Property quality. The lien is only as good as the property securing it. Vacant lots, condemned buildings, landlocked parcels, properties with environmental contamination, and homes in severe disrepair can all carry tax liens. If the owner does not redeem and you foreclose, you own what is there. A derelict property with a $3,000 lien and $45,000 in necessary remediation is not a windfall.

Hidden encumbrances. A tax lien is not automatically first in priority. Municipal liens, HOA assessments, and utility liens can survive the foreclosure process and attach to a property you now own. A thorough title search is not optional — it is the baseline.

Redemption uncertainty. Early redemption reduces your total interest income. Late or no redemption forces you into a foreclosure process that varies in cost, timeline, and complexity by state. Illinois, for example, has one of the highest statutory interest rates and also some of the most involved foreclosure procedures.

Competitive bidding. In liquid markets, institutional investors — banks, hedge funds, dedicated lien funds — systematically outbid individual investors or drive rates down to levels that compress returns significantly. The 16% rate in Arizona or 18% in Florida looks different when competitive pressure drives your actual yield to 4%.

Legal complexity. Tax lien law is state-specific and, within states, often county-specific. Redemption periods, foreclosure procedures, notification requirements, and lien priority rules vary enough that treating one state's system as representative of another is a reliable way to make expensive mistakes.

Who This Strategy Fits — and Who It Doesn't

Tax lien investing tends to work best for investors who are willing to treat it as a research-intensive, legally structured process rather than a passive income stream. That means studying state-specific law before entering any market, performing property-level due diligence on each certificate rather than bidding blind, understanding the foreclosure process in the jurisdiction before it becomes necessary, and managing a portfolio of liens to diversify the redemption and property risk across multiple assets.

It is poorly suited for investors who cannot or do not want to conduct that level of research, who need liquidity on a defined timeline, who lack access to local property records and inspection resources, or who are entering competitive metropolitan markets where institutional capital has largely compressed yields.

The investors who find consistent value in this space are typically methodical, locally knowledgeable, and operating in markets where retail competition remains viable — often smaller counties, less-followed states, or over-the-counter certificates that did not sell at auction.

Tax liens are a legitimate corner of the investment landscape — structured, legally defined, and in the right circumstances, a useful addition to a diversified approach to income generation.

But structured income is not the same as simple income. The structure that makes tax liens appealing — legal frameworks, statutory rates, property security — is also the structure that creates complexity, risk, and consequence. The same legal system that sets an 18% interest rate also defines the foreclosure process you will navigate if the owner does not pay, and the title issues you will encounter if the property has other claims against it.

Understanding the mechanism is not a prerequisite for investing in tax liens. It is the investment itself.

—

Claire West