The Substrate Beneath the Story

SpaceX is going public.

June 2026. $1.75 trillion - the largest IPO in history.

And by the time the ticker hits Nasdaq — the easy money will already be gone.

That's how it always works.

Peter Thiel got in before Facebook's IPO for $500,000.

His stake was worth $10 billion by the time the rest of us could buy a single share.

The insiders always eat first.

But this time, there's a way in.

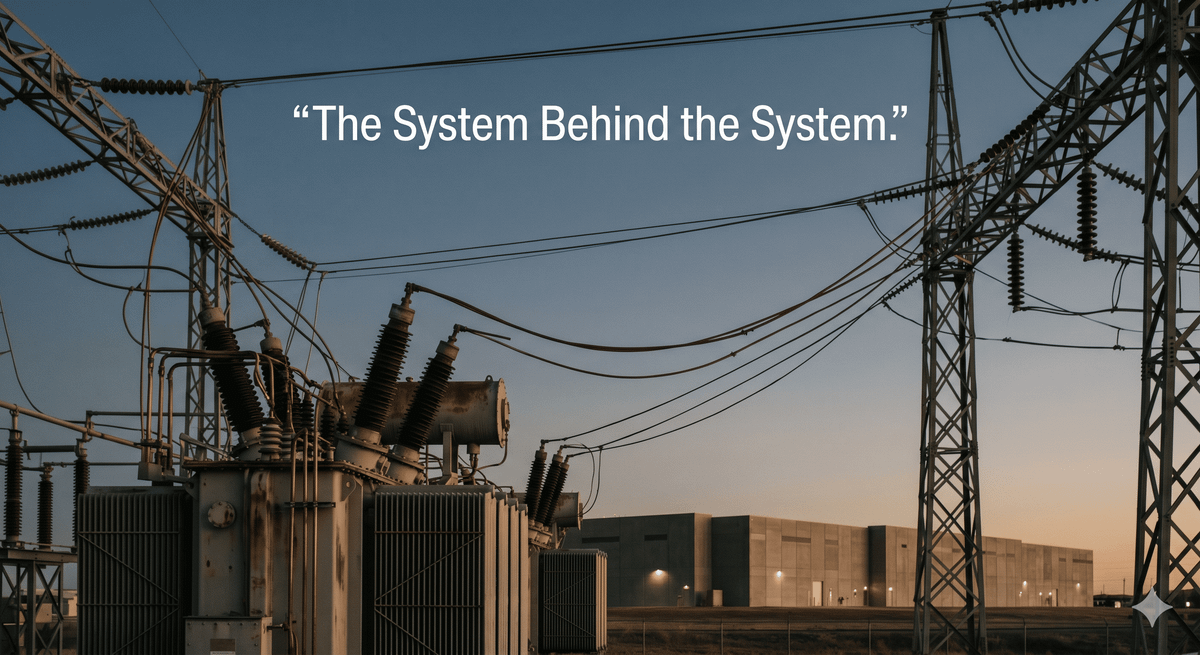

Elon Musk has a problem he doesn't talk about publicly.

He's building the world's largest AI supercomputer — a million GPUs, clustered inside a Memphis warehouse — and the US electrical grid cannot feed it.

Raw voltage from a transmission line would destroy the chips in a microsecond.

You need custom-engineered infrastructure to step that power down and distribute it safely.

Musk knows it. He said so himself:

"The next shortage will be voltage step-down transformers. You've got to feed the power to these things."

Lead times have gone from 20 weeks to over 120 weeks.

There is one small, publicly traded American company that can move fast enough to close that gap.

Wall Street hasn't noticed yet.

Their backlog just crossed $1.5 billion.

Five years ago, data centers were a rounding error in their revenue. Today, they're nearly half the business.

The last time Wall Street woke up this late to a story like this — Vertiv, the data center power play — the stock went from $10 to $180 in under two years.

This company is earlier in that same cycle.

And it's still priced like a boring industrial stock.

The full research — company name, ticker, buy-up-to price — is waiting for you.

Along with a free backdoor play you can buy in any brokerage account today, before a single page of the S-1 has been made public.

The filing is expected any day.

The details are here. →

The window is measured in weeks.

Breakthroughs Fail Where No One Is Looking

The interesting thing about major technological waves is not how they begin, but where they get stuck.

Ideas rarely run out. Capital rarely runs out. What runs out is power capacity, cooling water, skilled labor, transformer manufacturing slots, and access to the right piece of land near the right substation. Every generational technology story eventually becomes a story about physical limits — and the industries positioned at those limits tend to receive far less attention than the companies whose names appear on the announcement.

This is not a new pattern. It is the pattern. The question worth asking is what it looks like right now.

The Illusion of "Front-Running IPOs"

Public discussion of how to benefit from a technological wave tends to fixate on a specific moment: the initial public offering. The mental model is that being early means being close to the listing — or, if possible, ahead of it.

This framing misunderstands how modern capital markets function. Pre-IPO allocations in the highest-profile AI companies are largely absorbed by sovereign wealth funds, strategic partners, established venture firms, and a narrow tier of accredited investors with existing relationships. By the time shares become available to retail markets, early capital appreciation has typically already occurred in private rounds — often through multiple valuation step-ups before any public listing takes place.

The more durable access point is rarely the headline company itself. It is the collection of less-visible businesses that the headline company depends upon to operate. These firms are often already public, already priced by analysts, and often less volatile because their revenue is contractually tied to infrastructure buildouts rather than product adoption cycles.

The shift in framing matters. "How do I get in early on an AI company" is a timing question. "Which businesses are structurally necessary for this wave to continue" is an analytical one.

Infrastructure Reality

A large AI training cluster is sometimes described as "just a data center," but the physics and economics are categorically different from conventional computing infrastructure.

Traditional CPU-heavy server racks operate at 5 to 10 kilowatts. Modern AI clusters routinely push rack densities above 50 to 70 kilowatts, forcing a shift from conventional air cooling to direct-to-chip and immersion liquid systems. Power draw scales accordingly. Recent analyses of AI-focused facilities describe single training campuses requiring 100 to 300 megawatts per site, with multi-building complexes approaching the electrical load of a small city.

This changes the planning problem entirely. A conventional cloud data center could be sited flexibly and provisioned within industry-standard timelines. An AI training facility must be located where sufficient power can be delivered — not eventually, but on a construction schedule that matches compute demand. Operators are increasingly finding that the binding constraint is not chip availability, but grid interconnection.

The cooling layer has become its own discipline. Studies of immersion and liquid cooling for GPU datacenters describe closed-loop systems, precision leak detection, and PUE targets near 1.1, with water consumption and thermal management emerging as engineering problems of comparable weight to compute design itself.

When you zoom out, a training cluster is not a room full of clever chips. It is a coordinated physical machine for turning electricity and capital expenditure into model updates under strict thermal and networking constraints.

Visible Innovation vs. Hidden Infrastructure

| What the public watches | What the system actually depends on |

|---|---|

| New model releases and benchmark scores | Grid interconnection approvals, substation capacity, and long-duration power contracts iot-analytics+1 |

| Public debates over AI safety and ethics | Industrial-scale cooling systems, water availability, and thermal engineering acm+1 |

| High-profile AI company valuations | Semiconductor manufacturing capacity, leading-edge fab allocation, and advanced packaging trendforce |

| Consumer chatbots and productivity apps | Specialized networking fabrics (InfiniBand, high-speed Ethernet) that can represent capex comparable to compute hardware arxiv+1 |

| IPO announcements | Multi-year buildout cycles of power, land, and permitting already under way before any listing sanchez+1 |

Bottlenecks

The most underappreciated component in the AI infrastructure story is arguably the electrical transformer.

Large-scale data centers require high-voltage transformers to step grid power down to usable levels. Lead times for this equipment have extended significantly in recent years, pushing some orders two to three years forward. The manufacturing base is concentrated among a limited number of global suppliers, and capacity additions require years of their own. When transformer supply tightens, entire data center projects delay — regardless of how much capital has been committed.

Grid capacity is the second layer. Deloitte's analysis of U.S. infrastructure suggests that power demand from data centers alone could strain interconnection queues in multiple regions, requiring coordinated upgrades across generation, transmission, and distribution simultaneously. Utilities operating under traditional regulatory frameworks often need years to approve and construct new substations — time frames that sit awkwardly against the compressed cycles of AI compute demand.

The third layer is manufacturing lead times for critical specialized components: optical transceivers for high-speed networking, liquid cooling distribution units, specialized power distribution hardware, and advanced packaging for the accelerators themselves. These are not consumer categories. They are industrial supply chains with their own cadence, their own bottleneck dynamics, and their own pricing structures independent of end-customer AI adoption rates.

Case Lens: How Industrial Suppliers Quietly Become Critical

Every major technology cycle eventually reveals a second category of beneficiaries — not the companies building the product people see, but the companies supplying what that product requires to exist at scale.

In the railroad era, it was the steel mills and locomotive works. In the early internet era, it was the optical fiber and routing equipment vendors who profited even as many dot-com companies failed. In the smartphone cycle, it was the specialized suppliers of glass, sensors, battery cells, and radio-frequency components — many of them unfamiliar to consumers, but structurally essential to the devices.

The pattern in AI appears to be following a similar trajectory. Data center infrastructure market analyses indicate that capital expenditure on physical buildout — power, cooling, networking, and real estate — is expanding in parallel with, and in some cases ahead of, spending on the compute hardware itself. The companies engineering these systems are often decades-old industrial businesses with established customer relationships, long-duration contracts, and revenue models that do not depend on whether any particular AI application succeeds commercially.

This is not a glamorous story. It is an arithmetic one. The infrastructure layer of any large technology wave tends to consolidate among firms with demonstrated execution capability, existing manufacturing capacity, and credibility in multi-year procurement cycles. The companies that win in that layer are usually not the ones generating headlines.

Risk Lens

The infrastructure layer carries its own distinctive risks, and they are worth understanding as clearly as the opportunity.

Cyclicality. Data center buildout is capital-intensive and responsive to financing conditions. Interest rate shifts, credit cycles, and hyperscaler capex decisions can meaningfully delay or compress order books. Infrastructure suppliers whose revenue is concentrated among a small number of large customers are particularly exposed to this variance.

Overcapacity risk. The late-1990s telecom cycle demonstrated how quickly optimistic demand forecasts can produce durable overbuild. Estimates suggest that by 2001, only around 5 percent of installed fiber-optic capacity was in active use — despite substantial long-term strategic value of the underlying infrastructure. Equity holders in that cycle experienced severe losses even where the physical buildout proved valuable a decade later. The parallel for AI infrastructure is not that it will fail, but that its returns may be mistimed relative to current expectations.

Narrative mispricing. When a sector receives sustained attention, valuations across its supply chain can move in correlation regardless of individual firm fundamentals. Some infrastructure suppliers may be priced as if they are AI-exposed when their actual revenue is diversified across multiple end markets. Others may be genuinely AI-critical but priced too conservatively because their names lack the recognition of frontier model developers.

Regulatory and permitting exposure. Grid interconnection, environmental review, and water usage are increasingly political. Projects can be delayed or relocated based on state-level policy decisions that sit outside any supplier's control.

For investors and analysts working this layer, the question is not whether AI infrastructure will be built. It is whether the economics remain resilient across energy markets, credit cycles, and regulatory regimes.

The story of any technological cycle is told in two voices. The loud one is about products, personalities, and projections. The quiet one is about what had to be built for any of it to function.

AI is no exception. The models will continue to improve. The headlines will continue to compress complex developments into digestible narratives. And beneath all of it, a quieter industrial story will continue to unfold — one of substations and cooling manifolds, of manufacturing lead times and interconnection queues, of decades-old businesses that now find themselves structurally necessary to a technology cycle they did not originate.

The leverage in any wave is rarely where the attention points. It is in what the wave requires to continue. Understanding that distinction is the difference between following a story and understanding the system that makes the story possible.

—

Claire West