The Mechanism Is the Message

In 1934, the government executed a legal maneuver that transferred billions in wealth overnight.

Most Americans had no idea it was coming.

A small group who saw it early walked away wealthy.

Everyone else paid for it.

Trump has the same legal authority today. Advisors close to the administration believe he's considering using it. If he does, the transfer happens fast — and the window to be on the right side of it is already closing.

We put together a free report on exactly what this move is, why the timing points to now, and the one step ordinary Americans can take to position themselves before it happens.

It costs nothing. Takes 30 seconds to request.

The people who moved early in 1934 didn't have a warning.

You do.

Most Financial Shifts Are Recognized in Retrospect

There is a particular quality to major financial transitions: they are rarely announced in language that communicates their actual scale.

The words used at the time tend to be administrative. Stabilization. Adjustment. Revaluation. Emergency relief measure. The vocabulary of management, not transformation. And so most people — focused on the daily friction of economic life — process these events as technical policy matters and move on. The structural consequences reveal themselves years later, when balance sheets look permanently different and the explanation has been quietly absorbed into history.

Understanding how these tools work — not as dramatic events but as deliberate mechanisms — is the more useful frame. Not because history repeats exactly. But because the logic tends to.

The 1930s as a Structural Case Study

The sequence of actions in the United States between 1933 and 1934 is worth examining in precise terms, because the dramatics of the period tend to obscure the mechanics.

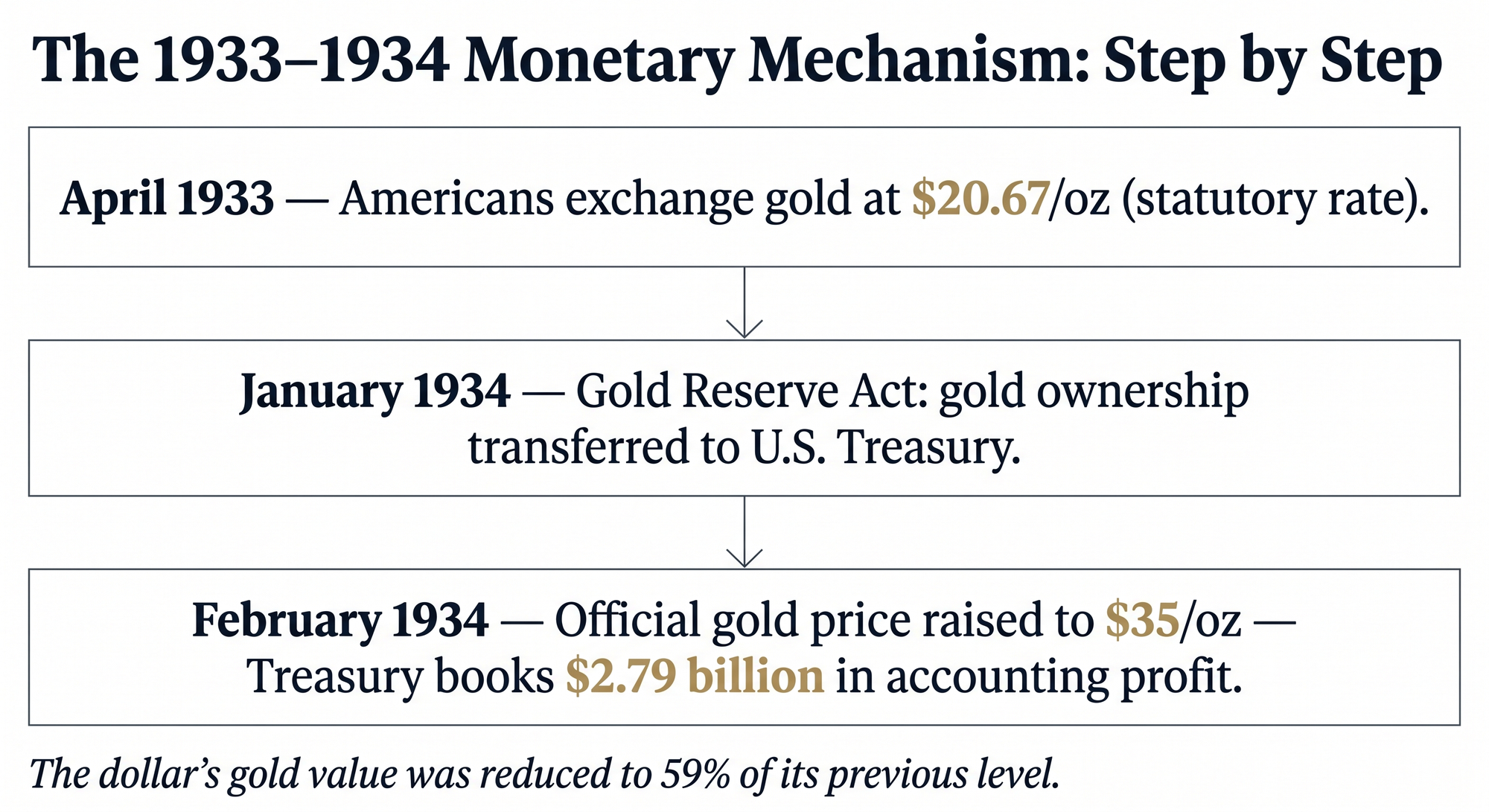

In April 1933, under Executive Order 6102, Americans were required to deliver most of their gold coins, bullion, and gold certificates to the Federal Reserve, receiving $20.67 per troy ounce in return — the statutory rate in place since 1900. This was legally a compensated exchange, not a seizure — though the terms of compensation were set entirely by the government, not the market.

Nine months later, the Gold Reserve Act of January 1934 transferred ownership of all monetary gold from the Federal Reserve to the U.S. Treasury. The president then revalued the price of gold from $20.67 to $35 per troy ounce — a change in the statutory price, not a market discovery. The dollar's gold value was thereby reduced to 59 percent of what it had been under the Gold Act of 1900.

The direct fiscal consequence was concrete: the revaluation generated an estimated $2.79 billion in Treasury profit — created not through taxation or borrowing, but through accounting repricing. $2 billion of that was placed into the Exchange Stabilization Fund, giving the Treasury direct capacity to manage currency values without Federal Reserve involvement.

Between 1933 and 1937, U.S. GNP grew at an average annual rate exceeding 8 percent. The causal chain is debated by economic historians. The mechanism, however, is not.

What Actually Changes in These Moments

The confusion in watching these events unfold — both then and now — comes from focusing on the announced action rather than the balance sheet effect.

When gold was revalued in 1934, what actually changed was the relationship between a fixed asset and all denominated claims against it. Debt contracted in old dollars was now repayable in devalued ones. The real burden of outstanding obligations declined. The money supply could expand. Import prices rose; export competitiveness improved. None of this required a vote on whether to "raise prices." It required changing one statutory number.

This is the essential character of monetary policy tools: they operate on valuations, not just flows. When a government adjusts an official price, a reserve requirement, an interest rate ceiling, or the rules governing what assets can be held in regulated accounts, it changes the landscape of every balance sheet simultaneously — without touching individual accounts directly.

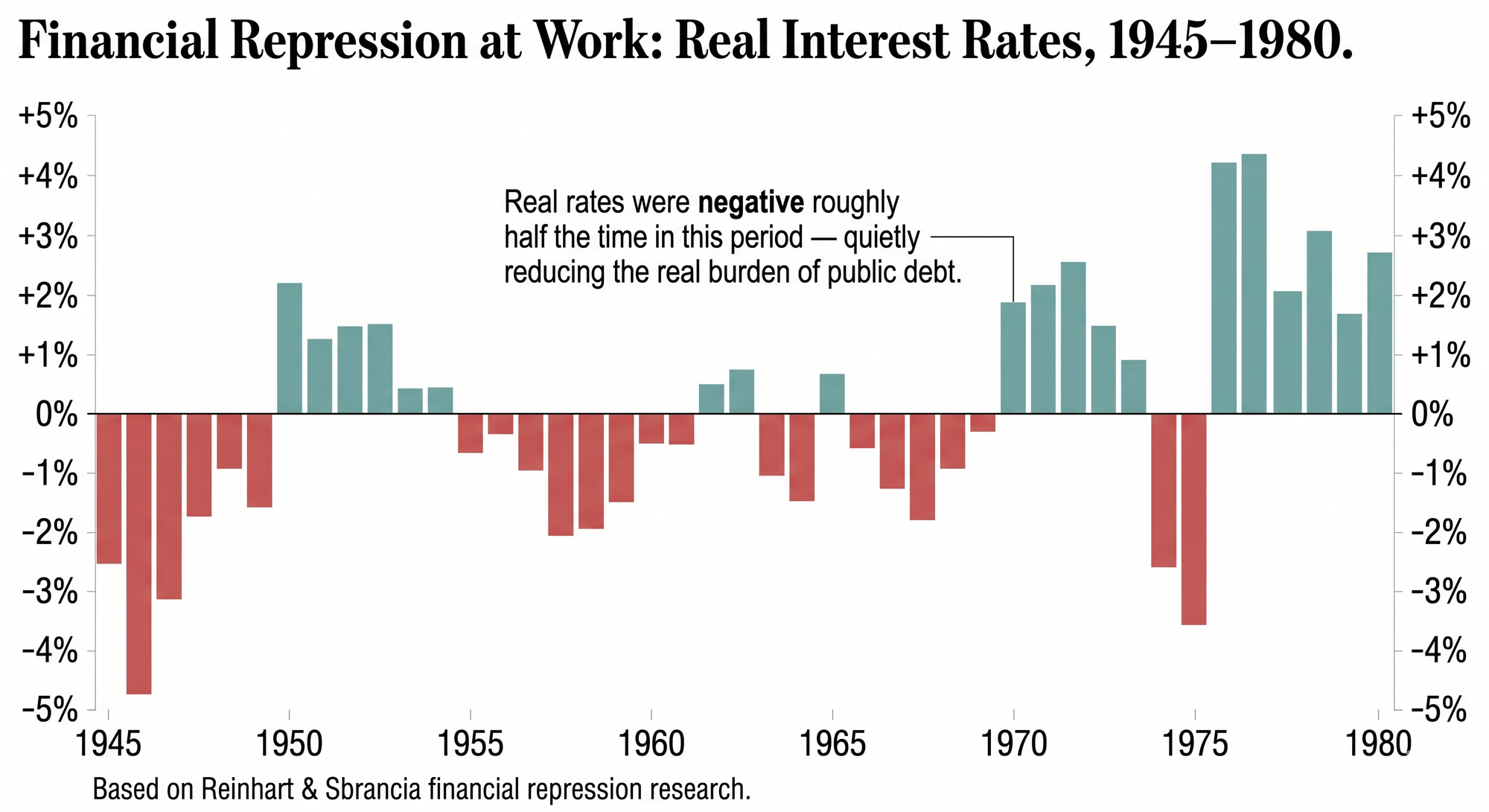

Carmen Reinhart's research on financial repression captures the post-World War II version of this logic precisely: by maintaining nominal interest rates below the rate of inflation, governments in advanced economies kept real interest rates negative roughly half the time between 1945 and 1980. This represented, in her framing, "a transfer from creditors to borrowers" — quiet, persistent, and enormously effective at reducing the real value of accumulated public debt.

Perceived Event vs. Actual Mechanism

| Perceived event | Actual mechanism |

|---|---|

| "The government collected gold in 1933" | Forced exchange at a statutory rate, followed by sovereign repricing — creating $2.79B in Treasury profit from accounting change nytimes+1 |

| "The dollar was stabilized in 1934" | Dollar devalued to 59% of its previous gold value; real burden of domestic debt reduced accordingly federalreservehistory+1 |

| "Post-WWII prosperity reduced government debt" | Financial repression: regulated interest rates kept real rates negative ~50% of the time from 1945–1980, quietly liquidating debt filosofiadeldebito+1 |

| "Quantitative easing was a crisis response tool" | Central bank asset purchases that suppressed long-duration yields, transferred duration risk to the public balance sheet, and expanded monetary base stlouisfed+1 |

| "Inflation is a consumer price problem" | Inflation with below-inflation interest rates is a transfer mechanism — from savers and fixed-income holders to debtors, including sovereigns carmenreinhart+1 |

Why Governments Use These Tools

The motivation is rarely ideological in the moment. It is usually arithmetic.

Governments accumulate debt through recessions, wars, and structural deficits. When debt service costs become systemically threatening — consuming an expanding share of revenue, crowding out productive spending, or undermining creditor confidence — the available adjustment mechanisms are limited. Tax increases are politically difficult and economically constrictive. Explicit default is costly across every dimension. And austerity, as post-2008 Europe demonstrated, can be self-defeating in the short run.

What remains is the monetary toolkit: inflation that erodes real debt value, financial repression that suppresses the interest cost of that debt, currency adjustment that redistributes the burden internationally, or asset repricing that generates sovereign profit through accounting rather than taxation.

The U.S. debt-to-GDP ratio currently stands at approximately 100 percent, with the Congressional Budget Office projecting it could reach 144 percent by 2034 under current legislation, and potentially 169 percent by 2055 under long-term spending projections. Interest payments are projected to average around 12 percent of federal revenues between 2025 and 2030. The arithmetic, in other words, has a pressure of its own — independent of which party controls the levers.

Why Most People Miss It

The gap between public perception and structural reality is not accidental — it reflects a rational allocation of attention.

Headlines track events: a signing, an announcement, a number. The mechanisms embedded in those events — the changes to official pricing schedules, reserve requirements, yield curve control regimes, or monetary base expansion rules — require familiarity with institutional frameworks that most people reasonably do not maintain. Financial literacy curricula focus on personal finance. Economics education tends toward theory. And the financial press, under constant deadline pressure, defaults to narrative rather than mechanism.

The result is that the tools most capable of reshaping long-term wealth — asset repricing, currency adjustment, real interest rate suppression — are least visible in the moment they are deployed.

Risk Lens: What Would Need to Be True Today

Any serious assessment of whether the 1930s monetary toolkit could be revisited requires acknowledging what has structurally changed.

Gold is no longer the monetary anchor. The Bretton Woods system that tied currencies to gold ended in 1971, and the current fiat system operates without a commodity constraint on money supply expansion. An official gold revaluation today would not change monetary mechanics the way it did in 1934 — though it would generate Treasury accounting profit, since the U.S. holds approximately 261 million troy ounces of gold still carried on official books at the post-1934 rate of $42.22 per ounce, not current market prices.

Financial repression, however, does not require a gold standard. It requires institutional capacity to maintain nominal rates below inflation — which was demonstrated extensively during 2020–2022, when real yields reached deeply negative territory across the developed world.

For a more systematic deployment, the preconditions would include: sustained fiscal pressure severe enough to make explicit adjustment politically infeasible; institutional capacity to maintain rate ceilings against market pressure; and sufficient domestic control over capital flows to prevent evasion. None of these are currently in place to the degree required. But none of them are structurally impossible either.

The purpose of understanding these mechanisms is not preparation for a crisis that may never arrive in familiar form.

It is the more general discipline of reading policy actions structurally rather than narratively. When official language describes a "stabilization fund," the question worth asking is: stabilization of what, for whose benefit, on whose balance sheet. When an asset is officially repriced, the question is: who held it before, and who holds the profit after.

Wealth cycles are shaped not by the events that dominate headlines but by the legal and institutional adjustments that quietly follow them. The reader who understands the mechanism — not the drama around it — is in a different position than the one who only encountered the announcement.

That difference is what financial literacy, at its most structural, is actually for.

—

Claire West